Buying auto insurance is one of the most important responsibilities every driver must fulfill. Not only is it a legal requirement in most regions, but it also provides crucial financial protection in case of accidents, theft, or damage. However, many people rush through the process of purchasing auto insurance, often focusing only on cost and ignoring other key factors. This can lead to costly mistakes, inadequate coverage, or difficulties during claims.

In this comprehensive guide, we’ll explore five common mistakes drivers make when purchasing auto insurance and explain how you can avoid them to secure the right policy that balances cost, protection, and peace of mind.

Why Auto Insurance Matters

Before diving into the mistakes, it’s important to understand why auto insurance is so essential:

-

Legal compliance: Most states and countries require drivers to carry a minimum level of insurance.

-

Financial protection: It covers expenses related to accidents, repairs, or medical bills.

-

Peace of mind: You don’t have to worry about covering large, unexpected costs after an accident.

-

Liability protection: Auto insurance shields you from lawsuits if you’re responsible for an accident.

Given its importance, purchasing the right auto insurance should never be taken lightly. Yet many drivers still make avoidable errors.

Mistake 1: Focusing Only on the Cheapest Premium

Why People Make This Mistake

The first thing most buyers look at when shopping for auto insurance is the premium—the amount you pay monthly or annually. While affordability is important, many drivers fall into the trap of thinking the cheapest policy is the best deal.

The Hidden Problem

The cheapest premium often comes with:

-

Minimal coverage limits

-

High deductibles

-

Exclusions that leave you unprotected

For example, a policy with only the minimum legal liability coverage may not protect you if you cause a serious accident. If the damages exceed your policy limits, you’ll have to pay the difference out of pocket.

How to Avoid It

-

Compare coverage, not just cost: Review what each policy actually covers before deciding.

-

Balance premium and protection: Choose a policy that fits your budget but still provides adequate liability, collision, and comprehensive coverage.

-

Ask about discounts: Many insurers offer safe driver discounts, bundling deals, or loyalty rewards that reduce costs without sacrificing protection.

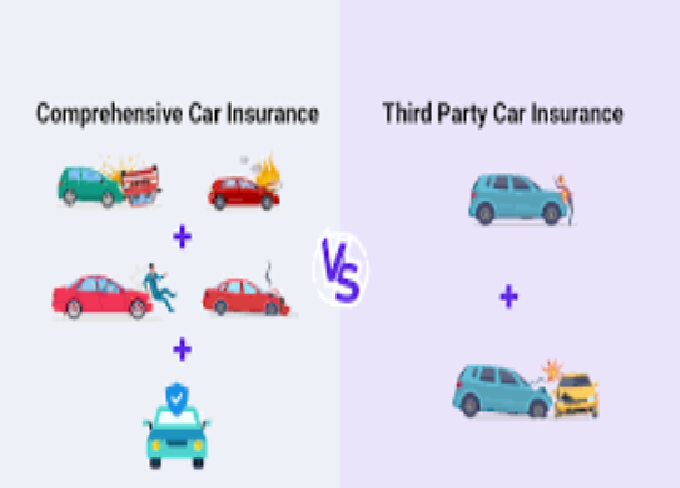

Mistake 2: Not Understanding Coverage Options

Why People Make This Mistake

Insurance terminology can be confusing, and many drivers skim through the details without fully understanding what they’re buying. This leads to either under-insuring or over-insuring their vehicle.

The Hidden Problem

Failing to understand coverage can result in:

-

Too little coverage: Leaving you exposed to high costs.

-

Redundant coverage: Paying for unnecessary add-ons you don’t need.

For example:

-

Liability insurance covers damage you cause to others but not your own vehicle.

-

Collision insurance covers your car in an accident, but not against theft or natural disasters.

-

Comprehensive insurance covers theft, vandalism, or weather-related damage.

If you don’t understand these differences, you may miss out on essential protection or waste money on extras.

How to Avoid It

-

Learn key coverage types: Understand liability, collision, comprehensive, personal injury protection, and uninsured motorist coverage.

-

Assess your needs: Consider your driving habits, the value of your car, and your financial situation.

-

Ask your agent: Don’t hesitate to ask for explanations in simple language.

Mistake 3: Providing Inaccurate or Incomplete Information

Why People Make This Mistake

In an effort to reduce premiums, some drivers may “forget” to mention certain details—like prior accidents, modifications, or the actual mileage driven. Others may simply make unintentional errors on their applications.

The Hidden Problem

Providing inaccurate or incomplete information can:

-

Invalidate your policy if the insurer finds out you lied.

-

Delay claims processing while the company verifies your details.

-

Lead to higher costs later if the insurer corrects your risk rating.

For example, if you claim you only drive 5,000 miles per year but actually drive 20,000, your insurer may deny a claim on the grounds of misrepresentation.

How to Avoid It

-

Be honest and transparent: Always provide accurate details about your driving history, car usage, and personal information.

-

Update your insurer regularly: If your circumstances change (new job, address, or vehicle), inform your provider.

-

Double-check applications: Make sure all details are correct before signing.

Mistake 4: Overlooking Deductibles and Policy Limits

Why People Make This Mistake

Many drivers focus on premiums but overlook how deductibles and policy limits impact their protection. This mistake often shows up at the worst time—during a claim.

The Hidden Problem

-

High deductibles: A lower premium often means a higher deductible. This means you’ll pay more out of pocket before insurance kicks in.

-

Low policy limits: Minimum legal coverage might not cover the full cost of accidents, especially if multiple vehicles or medical bills are involved.

For example, if your liability limit is $25,000 but you cause $60,000 in damages, you’ll have to cover the remaining $35,000.

How to Avoid It

-

Balance deductible and premium: Choose a deductible you can comfortably afford in case of an accident.

-

Review policy limits carefully: Consider raising your limits beyond the legal minimum for better protection.

-

Ask for scenarios: Request examples of how your coverage would apply in real-life accidents.

Mistake 5: Not Comparing Multiple Quotes

Why People Make This Mistake

Purchasing insurance can be time-consuming, and many drivers simply accept the first offer they receive—especially if it’s from a familiar company.

The Hidden Problem

By not shopping around, you may:

-

Miss out on better coverage at a lower price.

-

Overlook insurers offering better customer service or faster claims.

-

Fail to discover discounts available with other providers.

Auto insurance is highly competitive, and prices vary significantly between companies.

How to Avoid It

-

Get at least 3–5 quotes: Compare options from different insurers.

-

Use comparison tools: Online platforms can make this easier.

-

Evaluate more than cost: Look at coverage, customer reviews, and claims satisfaction ratings.

Additional Mistakes Many Drivers Overlook

While the above five are the most common, there are other pitfalls worth mentioning:

-

Not reviewing policies annually: Circumstances change—your insurance should too.

-

Failing to ask about discounts: You may qualify for savings you don’t know about.

-

Ignoring insurer reputation: Cheap premiums don’t matter if the company delays or denies claims.

-

Skipping optional coverages: Extras like roadside assistance or rental car reimbursement may be valuable depending on your lifestyle.

How to Choose the Right Auto Insurance Policy

To avoid these mistakes, follow a step-by-step approach:

-

Assess your needs: Evaluate your car’s value, your driving habits, and your financial situation.

-

Research coverage types: Understand liability, collision, comprehensive, and other options.

-

Gather multiple quotes: Compare not just premiums but also coverage and insurer reputation.

-

Review deductibles and limits: Ensure they are realistic for your budget.

-

Ask questions: Clarify anything you don’t understand before signing.

-

Review annually: Reassess your policy each year to adjust for changes.

Conclusion

Purchasing auto insurance may seem straightforward, but it’s full of potential pitfalls. By avoiding the five most common mistakes—focusing only on the cheapest premium, not understanding coverage, providing inaccurate information, overlooking deductibles and limits, and failing to compare quotes—you can make a smarter, more informed decision.

Auto insurance isn’t just about meeting legal requirements—it’s about protecting your financial well-being, your family, and your peace of mind. Taking the time to understand your options, review your policy carefully, and choose the right provider will ensure you have reliable protection when you need it most.