Life insurance is one of the most important financial tools for protecting your family’s future. It provides a safety net, ensuring that your loved ones won’t face financial hardship in the event of your untimely death. However, one of the most common questions people have is: “How much life insurance coverage do I really need?”

The answer is not the same for everyone. It depends on your financial obligations, income, lifestyle, and long-term goals. This article will guide you through the factors to consider, methods for calculating your needs, and common mistakes to avoid—so you can make an informed decision about the right level of coverage.

Understanding the Purpose of Life Insurance

Before calculating how much coverage you need, it’s essential to understand what life insurance is designed to do. At its core, life insurance provides financial protection for your dependents if you are no longer there to support them. It helps replace lost income, pay off debts, cover everyday living expenses, and fund long-term goals such as education or retirement.

Some of the most common reasons people buy life insurance include:

-

Protecting family income and maintaining their lifestyle.

-

Paying off a mortgage or other debts.

-

Covering final expenses like funeral and medical bills.

-

Ensuring children’s education is funded.

-

Leaving a financial legacy or inheritance.

The right amount of coverage ensures that all these needs are met without leaving your loved ones in financial distress.

Why “One-Size-Fits-All” Doesn’t Work

A common misconception is that everyone needs the same amount of life insurance. Many insurance agents or financial websites suggest simple formulas like “10 times your annual income”. While these rules of thumb are a good starting point, they don’t account for individual circumstances.

For example:

-

A 25-year-old with no children and little debt doesn’t need as much coverage as a 40-year-old with a mortgage, two kids, and a spouse who relies on their income.

-

Someone with significant savings and investments may require less coverage compared to someone with limited assets.

That’s why personal evaluation is essential to determine the right amount of life insurance for you.

Key Factors to Consider When Determining Coverage

Several financial and personal factors play into the decision of how much coverage you need. Let’s break them down:

1. Your Income and Replacement Needs

The primary role of life insurance is income replacement. If your family depends on your earnings, you’ll want coverage that replaces your income for a reasonable number of years.

-

Many experts suggest 10–15 years of income replacement.

-

For example, if you earn $50,000 annually, you may need $500,000–$750,000 in coverage.

2. Debts and Liabilities

Outstanding debts can burden your family if you’re not there to pay them off. Consider:

-

Mortgage balance.

-

Car loans.

-

Student loans.

-

Credit card balances.

Your policy should ideally be enough to clear these debts so your loved ones don’t inherit them.

3. Family Size and Dependents

The number of people who rely on your income affects coverage needs. A single person without dependents may only need minimal coverage, while a married parent with three young children may need significantly more.

4. Education and Future Expenses

If you want to fund your children’s college education or other milestones (like weddings), include those costs in your coverage estimate. Education expenses can easily range from tens of thousands to hundreds of thousands of dollars.

5. Lifestyle and Standard of Living

Think about the lifestyle you want your family to maintain. Do you want them to stay in the same home, travel, or pursue hobbies and passions? Adjust your coverage accordingly.

6. Savings, Investments, and Other Assets

Existing assets reduce the amount of coverage you need. If you already have a large emergency fund, retirement savings, or investments, these can offset some of the coverage requirements.

7. Existing Insurance Policies

Don’t forget to account for any existing coverage, such as group life insurance through your employer. While employer-provided policies are often smaller (1–2 times salary), they still reduce the gap you need to fill.

Methods for Calculating Life Insurance Needs

There are several methods to calculate how much coverage you need. Each has pros and cons, and the best choice depends on your situation.

1. Income Replacement Method

This method multiplies your annual income by a factor (usually 10 to 15).

-

Example: If you earn $60,000 annually, you’d need $600,000–$900,000 in coverage.

Pros: Simple, quick estimate.

Cons: Doesn’t consider debts, assets, or specific goals.

2. DIME Formula (Debts, Income, Mortgage, Education)

This popular method breaks coverage into four categories:

-

D (Debts): Pay off all personal debts and final expenses.

-

I (Income): Multiply your annual income by the number of years your family needs support.

-

M (Mortgage): Cover your home loan balance.

-

E (Education): Add future education costs for children.

Example:

-

Debts: $20,000

-

Income (10 years × $70,000): $700,000

-

Mortgage: $200,000

-

Education: $100,000

Total Coverage Needed: $1,020,000

3. Human Life Value Approach

This method calculates the economic value of your life in terms of future earnings.

-

Estimate your annual income.

-

Subtract taxes and personal expenses.

-

Multiply by the number of years until retirement.

Example:

-

Annual income: $80,000

-

Personal expenses and taxes: $20,000

-

Net contribution to family: $60,000

-

Years until retirement: 25

Coverage Needed: $1,500,000

4. Needs-Based Approach

This is the most personalized method. You list all expenses your family would face and subtract assets they already have. The remainder is your coverage need.

Formula: Coverage = (Total Expenses + Future Goals) – (Existing Assets + Insurance).

Example Scenarios

Let’s look at different life stages to see how needs vary.

Young Single Adult

-

Few debts, no dependents.

-

May only need coverage for funeral costs and small debts.

-

$50,000–$100,000 could be sufficient.

Young Couple Without Children

-

Coverage should replace income and pay off debts.

-

Each partner may need 5–10 times income in coverage.

Married with Young Children

-

Highest need stage.

-

Coverage must include income replacement, mortgage, education, and lifestyle expenses.

-

Often $500,000–$2,000,000 depending on income and expenses.

Middle-Aged with Grown Children

-

Debts may be lower; children are financially independent.

-

Focus shifts to covering spouse’s income needs and retirement savings.

Retired Seniors

-

Usually need less coverage.

-

Coverage often intended for final expenses, estate planning, or leaving an inheritance.

Common Mistakes People Make

When deciding how much coverage to buy, avoid these mistakes:

1. Underestimating Expenses

Many people only think about big debts like a mortgage, forgetting ongoing living expenses like groceries, healthcare, and utilities.

2. Overreliance on Employer Coverage

Group life insurance is rarely enough and often ends if you change jobs.

3. Not Updating Coverage

Life insurance needs change as you move through life stages. Review your coverage every few years.

4. Forgetting Inflation

Future costs will be higher due to inflation. A college education that costs $50,000 today could cost double in 15 years.

5. Ignoring Spouse’s Needs

Even if your spouse works, they may need extra support if you pass away, especially if childcare responsibilities increase.

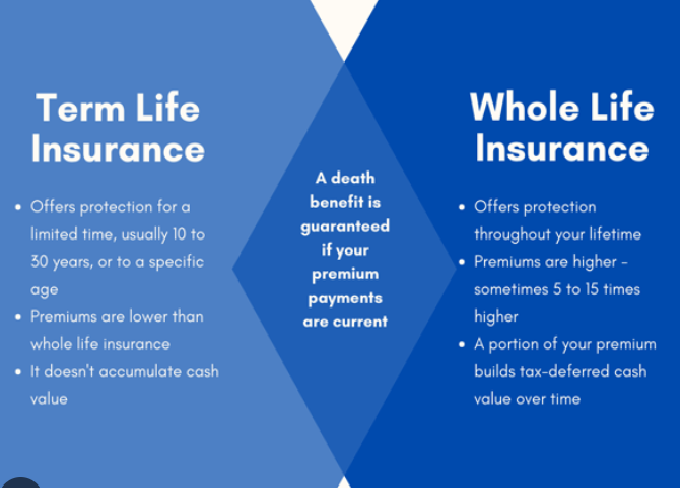

Term vs. Permanent Insurance: Does It Affect Coverage?

The amount of coverage you need isn’t the only decision—you must also choose the type of policy.

-

Term Life Insurance: Provides coverage for a specific period (10, 20, or 30 years). Affordable and suitable for income replacement during high-need years.

-

Permanent Life Insurance: Lasts for your lifetime and includes a cash value component. More expensive but can be part of long-term financial planning.

For most people, term insurance offers the best balance of affordability and sufficient coverage. Permanent insurance may make sense for estate planning or wealth transfer.

How to Review and Adjust Coverage Over Time

Life doesn’t stay the same, and neither should your life insurance coverage. Major life events are good times to reassess your policy:

-

Marriage or divorce.

-

Birth or adoption of a child.

-

Buying a home.

-

Starting or selling a business.

-

Retirement planning.

A general rule is to review your coverage every 3–5 years or whenever a major financial change occurs.

Professional Guidance and Tools

You don’t have to figure it out alone. Several resources can help:

-

Online Calculators: Many insurers and financial websites offer life insurance calculators.

-

Financial Advisors: Professionals can help you analyze your income, debts, and goals.

-

Insurance Agents: They can guide you through policy options and ensure you’re neither under- nor over-insured.

Conclusion

Life insurance isn’t just about numbers—it’s about peace of mind. The right coverage ensures that your loved ones will have financial security even if you’re no longer there to provide for them. While rules of thumb like “10 times your income” can be helpful starting points, the best approach is to tailor your coverage to your unique needs, debts, goals, and family situation.

By considering income replacement, debts, dependents, future expenses, and existing assets, you can arrive at a realistic figure that safeguards your family’s future. And remember—life insurance needs change over time, so reviewing and updating your policy regularly is just as important as buying it in the first place.

Ultimately, the question isn’t just “How much life insurance do you need?” but “How much peace of mind do you want to give your family?”