Life insurance is one of the most important financial tools available to protect your loved ones and ensure financial stability in times of uncertainty. Unfortunately, many people either delay purchasing coverage, underestimate how much they need, or make decisions without fully understanding the implications. These mistakes can leave families financially vulnerable when tragedy strikes.

This article explores the top mistakes to avoid when buying life insurance, helping you make informed decisions and secure the right policy for your future.

1. Delaying the Purchase of Life Insurance

One of the biggest mistakes people make is waiting too long to buy life insurance. Many believe they are “too young” or “too healthy” to need coverage, or they postpone the decision until later in life.

-

Why it’s a mistake:

The younger and healthier you are, the cheaper your premiums will be. Waiting until you are older—or until health issues develop—can make life insurance much more expensive or even impossible to obtain. -

Better approach:

Purchase life insurance as soon as you have financial dependents, debts, or other obligations. Locking in a policy early ensures long-term affordability and guaranteed protection.

2. Underestimating How Much Coverage You Need

Another common error is buying too little coverage. Many people opt for the cheapest policy or choose a random amount without calculating their family’s true financial needs.

-

Why it’s a mistake:

If your coverage isn’t sufficient, your family may struggle to pay the mortgage, handle daily expenses, or fund education after your passing. -

Better approach:

A good rule of thumb is to buy coverage equal to 10–15 times your annual income. Consider future expenses such as children’s education, outstanding debts, and long-term living costs. Using a life insurance calculator or consulting a financial advisor can help you choose the right amount.

3. Overestimating Employer-Provided Life Insurance

Employer-sponsored life insurance is a great benefit, but relying solely on it can be a major mistake.

-

Why it’s a mistake:

Group life insurance provided by employers is often limited—usually one or two times your annual salary. This is rarely enough to cover your family’s needs. Additionally, if you change jobs or lose employment, you may lose your coverage altogether. -

Better approach:

Use employer-provided coverage as a supplement, not your primary plan. Secure an individual policy that you control and can keep regardless of your job status.

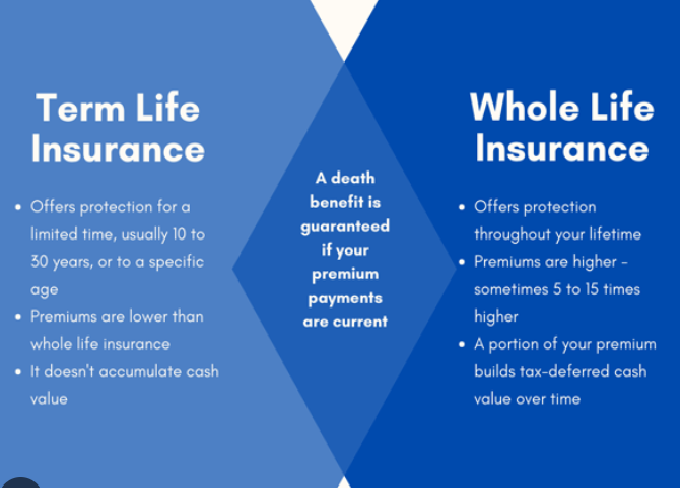

4. Choosing the Wrong Type of Life Insurance

Life insurance isn’t one-size-fits-all. Many buyers purchase a policy without understanding the difference between term life insurance and permanent life insurance.

-

Why it’s a mistake:

Choosing the wrong type of policy could leave you overpaying for coverage you don’t need, or worse, without coverage when you need it most. -

Better approach:

-

Term life insurance is affordable and suitable for temporary needs (e.g., until kids are grown or a mortgage is paid off).

-

Permanent life insurance (whole life, universal life, etc.) provides lifelong protection and builds cash value but comes at a higher cost.

Evaluate your financial goals before deciding.

-

5. Focusing Only on Price, Not Value

Many buyers go straight for the cheapest policy without considering what they’re actually getting.

-

Why it’s a mistake:

The cheapest policy may exclude important riders, offer insufficient coverage, or be from an insurer with poor customer service or claim settlement history. -

Better approach:

Balance affordability with value. Research the insurer’s reputation, claim settlement ratio, and policy features. Remember, the goal is to provide financial security—not just save a few dollars.

6. Not Disclosing Accurate Health Information

Some applicants hide medical conditions, smoking habits, or lifestyle risks to get cheaper premiums.

-

Why it’s a mistake:

Insurance companies conduct medical exams and background checks. If you withhold information, the insurer can deny your claim later, leaving your family unprotected. -

Better approach:

Always be honest about your health and lifestyle. You might pay slightly higher premiums, but your family will be protected when they need it most.

7. Ignoring Riders and Additional Benefits

Life insurance riders are optional add-ons that enhance your policy. Many buyers ignore them or are unaware of their benefits.

-

Why it’s a mistake:

Without riders, you may miss out on valuable protections such as critical illness coverage, accidental death benefits, or waiver of premium. -

Better approach:

Review available riders and choose those that align with your needs. For example:-

Critical illness rider provides financial support if you’re diagnosed with a serious illness.

-

Accidental death benefit rider increases payout if death occurs due to an accident.

-

Waiver of premium rider ensures your policy remains active even if you can’t pay premiums due to disability.

-

8. Buying Without Comparing Multiple Policies

Some buyers purchase the first policy offered by an agent without exploring other options.

-

Why it’s a mistake:

You might miss out on better coverage, lower premiums, or additional features. Different insurers have different underwriting rules and pricing structures. -

Better approach:

Compare policies from at least three different insurers. Use online comparison tools, consult financial advisors, and read policy documents carefully before deciding.

9. Naming the Wrong Beneficiary

Beneficiary designation is one of the most critical steps in buying life insurance. Yet, many people either forget to name a beneficiary, name a minor child, or fail to update beneficiaries after major life events.

-

Why it’s a mistake:

If no beneficiary is listed, the payout may go into your estate, causing delays, legal complications, and taxes. Naming a minor directly can also create issues since minors cannot legally manage large sums of money. -

Better approach:

-

Always designate at least one primary and one contingent beneficiary.

-

Update beneficiaries after marriage, divorce, or the birth of a child.

-

Consider setting up a trust if you want to leave money for minors.

-

10. Not Reviewing the Policy Regularly

Life insurance is not a “set it and forget it” purchase. Your financial situation and family responsibilities will change over time.

-

Why it’s a mistake:

If you don’t review your policy, you may end up with inadequate coverage, outdated beneficiaries, or missed opportunities for better plans. -

Better approach:

Review your policy every 2–3 years or after major life events such as marriage, having children, buying a home, or changing jobs. Adjust coverage as needed.

11. Canceling a Policy Too Soon

Some people cancel their life insurance policies due to financial struggles or because they think they no longer need coverage.

-

Why it’s a mistake:

Canceling your policy may leave your family without protection. Reapplying later may result in higher premiums due to age or health issues. -

Better approach:

Before canceling, explore alternatives such as reducing coverage, switching to a term policy, or using policy loans in permanent insurance.

12. Not Considering Inflation

Inflation erodes the value of money over time, and many people don’t factor this in when choosing coverage amounts.

-

Why it’s a mistake:

A policy worth $500,000 today may not have the same impact 20 years later when costs of living, education, and healthcare are much higher. -

Better approach:

Choose a policy with increasing coverage options or buy more coverage upfront to account for inflation.

13. Assuming All Insurers Are the Same

Some buyers believe that all insurance companies provide the same service and reliability.

-

Why it’s a mistake:

Insurers differ in claim settlement ratios, financial strength, customer service, and additional features. Choosing a poorly rated company could put your family’s future at risk. -

Better approach:

Research each insurer’s financial ratings (from agencies like AM Best or Moody’s) and claim settlement history. Pick a reputable company with a strong record.

14. Overlooking Policy Exclusions

Every life insurance policy comes with exclusions—situations where the insurer won’t pay the death benefit.

-

Why it’s a mistake:

Failing to read exclusions can leave your family shocked when a claim is denied. Common exclusions include suicide within the first two years, death due to risky hobbies, or non-disclosure of health issues. -

Better approach:

Carefully read the fine print and ask your agent to explain exclusions. Make sure you’re comfortable with the terms before buying.

15. Buying Without Professional Guidance

Many people purchase policies without consulting a financial advisor or insurance expert.

-

Why it’s a mistake:

Without expert input, you may choose the wrong type of policy, inadequate coverage, or miss out on cost-saving opportunities. -

Better approach:

Consult a licensed financial advisor or insurance professional who can assess your unique situation and recommend the most suitable policy.

Conclusion

Buying life insurance is one of the most important financial decisions you’ll ever make. But mistakes—such as delaying purchase, underestimating coverage, relying solely on employer insurance, or failing to update beneficiaries—can undermine your family’s financial protection.

By understanding these top mistakes to avoid when buying life insurance and following best practices, you can ensure your loved ones are financially secure, no matter what the future holds. Life insurance isn’t just about peace of mind—it’s about responsibility, foresight, and leaving a legacy of protection.