Life insurance is one of the most important financial tools available today. It is designed to provide financial protection to your loved ones in the event of your death, ensuring that they have the means to cover living expenses, debts, or long-term financial goals. However, choosing the right life insurance policy can be confusing because of the wide variety of options available. From term life to whole life, each type of policy serves different needs. In this guide, we will break down the different types of life insurance, explore the benefits, and give you practical tips on how to choose the right policy for your situation.

What is Life Insurance?

Life insurance is a contract between you (the policyholder) and an insurance company. In exchange for premium payments, the insurance company promises to pay a lump sum (called the death benefit) to your beneficiaries upon your death.

This death benefit can serve several purposes, such as:

-

Covering funeral expenses

-

Paying off debts like mortgages or loans

-

Replacing lost income for your family

-

Funding your children’s education

-

Providing long-term financial security

Life insurance essentially acts as a safety net, ensuring that your dependents won’t face financial hardship when you are no longer there to provide for them.

Why is Life Insurance Important?

Many people underestimate the value of life insurance until it’s too late. Here are some reasons why it’s crucial:

-

Income Replacement – If you are the main breadwinner in your family, your death could leave your dependents financially vulnerable. Life insurance ensures they can maintain their lifestyle.

-

Debt Protection – Mortgages, car loans, and credit card balances don’t vanish after your death. A life insurance policy can cover these obligations.

-

Estate Planning – Life insurance can provide liquidity for estate taxes and ensure smooth wealth transfer to heirs.

-

Peace of Mind – Knowing your loved ones are financially secure, even in your absence, brings emotional comfort.

Types of Life Insurance

Life insurance is not a one-size-fits-all product. The right policy depends on your age, income, health, and long-term goals. Let’s look at the major types of life insurance available:

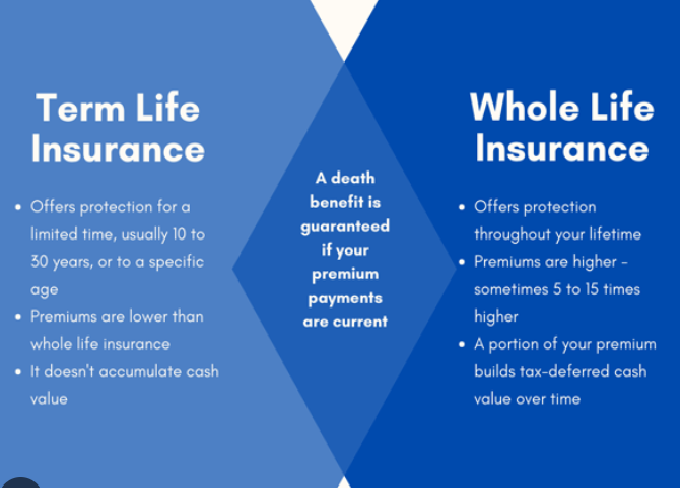

1. Term Life Insurance

Term life insurance is the most straightforward and affordable option. It provides coverage for a specific period—typically 10, 20, or 30 years. If the insured person dies during the term, the beneficiaries receive the death benefit. If the term expires while the insured is still alive, no payout is made.

Key Features:

-

Affordable premiums

-

Fixed coverage period

-

No cash value component

Best For: Young families, individuals with temporary financial obligations (like mortgages), and those who want affordable protection.

2. Whole Life Insurance

Whole life insurance is a type of permanent life insurance that provides lifelong coverage. It also includes a savings component called “cash value,” which grows over time on a tax-deferred basis.

Key Features:

-

Lifetime coverage

-

Fixed premiums

-

Cash value that can be borrowed against

Best For: People seeking both protection and a long-term savings tool, or those involved in estate planning.

3. Universal Life Insurance

Universal life insurance is another form of permanent insurance, but it offers more flexibility than whole life. Policyholders can adjust their premiums and death benefits over time.

Key Features:

-

Flexible premiums

-

Adjustable death benefit

-

Cash value growth tied to interest rates

Best For: Individuals who want lifelong coverage but also the flexibility to change premiums and benefits.

4. Variable Life Insurance

Variable life insurance combines permanent coverage with investment opportunities. The policyholder can allocate cash value into different investment accounts like stocks, bonds, or mutual funds.

Key Features:

-

Investment component with potential for higher returns

-

Risk of loss depending on market performance

-

Lifelong coverage

Best For: People comfortable with investment risks and seeking higher growth potential.

5. Indexed Universal Life Insurance (IUL)

IUL is similar to universal life but ties cash value growth to a stock market index like the S&P 500. It provides opportunities for growth while offering a minimum guaranteed interest rate.

Key Features:

-

Growth linked to stock market indexes

-

Guaranteed minimum interest rate

-

Flexible premiums and benefits

Best For: Policyholders who want growth potential with less risk than variable life insurance.

6. Final Expense Insurance

Also known as burial insurance, this policy is designed to cover funeral costs, medical bills, and other end-of-life expenses.

Key Features:

-

Smaller death benefits (usually $5,000–$25,000)

-

Easy approval, often without medical exams

-

Affordable premiums

Best For: Seniors who want to ease the financial burden of funeral costs for their families.

7. Group Life Insurance

Many employers offer group life insurance as part of their benefits package. Coverage is usually limited and ends when you leave the job.

Key Features:

-

Offered through employers

-

Lower premiums due to group rates

-

Limited coverage amount

Best For: Employees seeking basic coverage at low cost, though it’s often best to supplement with an individual policy.

Benefits of Life Insurance

Having life insurance provides multiple advantages beyond financial protection. Let’s break down the benefits:

1. Financial Security for Loved Ones

The most obvious benefit is providing money to your dependents. It ensures that your spouse, children, or aging parents are financially secure after your passing.

2. Debt and Loan Coverage

Life insurance can pay off mortgages, car loans, personal loans, and even student debt, preventing creditors from burdening your family.

3. Wealth Transfer and Estate Planning

High-net-worth individuals use life insurance to pass wealth efficiently to the next generation while avoiding hefty estate taxes.

4. Tax Advantages

-

Death benefits are usually tax-free.

-

Cash value in permanent policies grows tax-deferred.

-

Some policies allow tax-free loans against the cash value.

5. Business Protection

Business owners can use life insurance for key person insurance or buy-sell agreements, ensuring the company continues smoothly if an owner or partner dies.

6. Retirement Planning Supplement

Some permanent life insurance policies build cash value, which can be used as an additional retirement income stream.

How to Choose the Right Life Insurance

Selecting the right life insurance policy requires careful consideration of your financial situation, goals, and family needs. Here’s a step-by-step approach:

Step 1: Assess Your Financial Needs

Ask yourself:

-

How much income would my family need if I die?

-

Do I have outstanding debts or mortgages?

-

Do I want to leave money for children’s education or other goals?

A common rule of thumb is to have life insurance coverage worth 10–15 times your annual income.

Step 2: Choose the Type of Policy

-

If affordability is your top concern → Term Life Insurance

-

If you want lifelong coverage with savings → Whole or Universal Life Insurance

-

If you want investment opportunities → Variable Life Insurance

-

If you only want to cover burial costs → Final Expense Insurance

Step 3: Compare Premiums and Coverage

Get quotes from multiple insurance providers. Don’t just focus on the cheapest option—look for a balance of affordability, benefits, and reliability.

Step 4: Evaluate the Insurance Company

Choose a reputable company with strong financial ratings. Look at customer reviews, claim settlement ratio, and service quality.

Step 5: Review Policy Riders

Riders are add-ons that enhance your policy. Popular riders include:

-

Critical illness rider – Pays out if diagnosed with a major illness.

-

Accidental death benefit – Extra payout if death is due to an accident.

-

Waiver of premium rider – Waives premiums if you become disabled.

Step 6: Seek Professional Advice

Insurance agents or financial advisors can help you select the best policy. Just be cautious of sales-driven advice—always do your own research too.

Common Mistakes to Avoid When Buying Life Insurance

-

Underestimating Coverage Needs – Many people buy too little coverage, leaving their families vulnerable.

-

Delaying Purchase – Premiums rise as you age or if health declines. Buying earlier saves money.

-

Relying Only on Employer Coverage – Group life insurance ends when you leave your job. Always have personal coverage.

-

Not Reviewing Policies Regularly – Life changes (marriage, kids, debt) may require more coverage.

-

Focusing Only on Price – Cheapest isn’t always best; balance affordability with long-term benefits.

Frequently Asked Questions (FAQs)

Q1: Is life insurance worth it if I’m single?

Yes, especially if you have debts, aging parents, or want to lock in low premiums at a young age.

Q2: Can I have more than one life insurance policy?

Absolutely. Many people combine employer coverage with individual policies for better protection.

Q3: What happens if I stop paying premiums?

Your policy may lapse. Some permanent policies allow you to use cash value to cover premiums temporarily.

Q4: Is the payout guaranteed?

As long as you pay premiums and the policy is active, the insurer must pay the death benefit.

Conclusion

Life insurance is more than just a financial product—it’s a promise of security and stability for the people you care about most. By understanding the types of life insurance, their benefits, and the steps to choose the right policy, you can make a smart decision that protects your loved ones for years to come.

Whether you’re just starting a family, building wealth, or planning for retirement, life insurance should be a cornerstone of your financial plan. The key is to evaluate your needs, compare options, and choose a policy that fits your unique situation.

In the end, life insurance is not about you—it’s about the people who depend on you.