Health insurance has become one of the most critical aspects of financial planning and personal well-being in today’s world. With the rising costs of healthcare, having an insurance plan provides individuals with financial protection and peace of mind during medical emergencies. However, choosing the right type of insurance plan can be confusing, especially when it comes to comparing private health insurance and government health insurance.

Both serve the same ultimate purpose—to provide coverage for medical expenses—but they differ significantly in terms of coverage options, cost, accessibility, flexibility, and eligibility. This article provides a comprehensive breakdown of the differences between private and government health insurance plans, helping you make an informed choice that fits your personal and family needs.

Understanding Health Insurance Basics

Before diving into the differences, it is essential to understand what health insurance is and why it matters. Health insurance is a contract between an individual and an insurance provider (either private or government-based) that covers part or all of the medical expenses in exchange for premium payments.

Key elements of any health insurance plan include:

-

Premiums: The amount you pay monthly or annually to keep your insurance active.

-

Deductibles: The out-of-pocket costs you must pay before insurance coverage starts.

-

Copayments/Coinsurance: A share of medical costs you are responsible for paying.

-

Coverage: The types of healthcare services included in the plan (hospitalization, prescription drugs, preventive care, etc.).

With this foundation, let’s examine the distinct features of private and government health insurance plans.

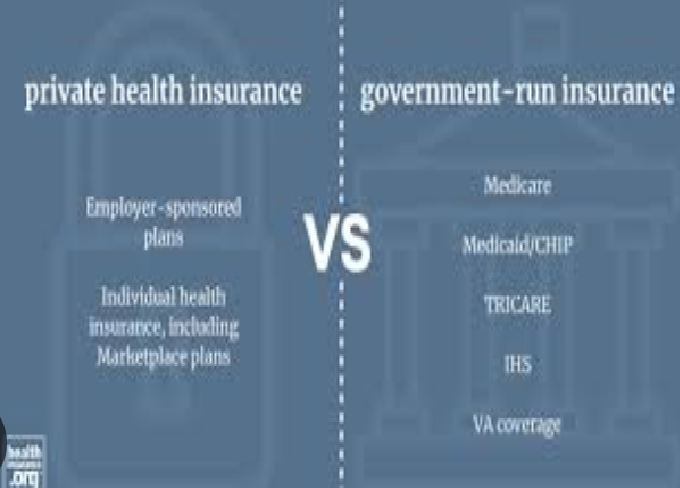

What Is Private Health Insurance?

Private health insurance is offered by private companies, employers, or organizations. Individuals can purchase these plans directly or receive them through workplace benefits.

Key Features of Private Health Insurance:

-

Variety of Plans: Options such as HMOs (Health Maintenance Organizations), PPOs (Preferred Provider Organizations), and high-deductible health plans (HDHPs).

-

Customization: Plans can be tailored to suit personal or family health needs.

-

Faster Access to Care: Often provides quicker access to specialists and elective procedures.

-

Broader Choice of Providers: Policyholders can often choose from a larger network of hospitals and doctors.

-

Higher Costs: Premiums and out-of-pocket costs are generally higher compared to government plans.

What Is Government Health Insurance?

Government health insurance is provided or subsidized by the state to ensure healthcare access for vulnerable populations or the general public. Examples include Medicare, Medicaid, national health schemes, or state-subsidized insurance programs (depending on the country).

Key Features of Government Health Insurance:

-

Publicly Funded: Financed through taxes, payroll deductions, or government funding.

-

Low or No Premiums: Often more affordable than private insurance.

-

Basic Coverage: Typically covers essential health services but may exclude advanced or luxury care options.

-

Eligibility-Based: Some programs are limited to certain groups (e.g., low-income individuals, elderly, disabled).

-

Longer Waiting Times: Patients may face longer waits for non-emergency treatments.

Cost Comparison Between Private and Government Plans

One of the biggest differences lies in costs.

-

Private Health Insurance:

-

Higher premiums, especially for comprehensive coverage.

-

Deductibles and copayments can be significant.

-

Costs vary depending on age, health status, location, and coverage type.

-

Example: In the U.S., private insurance premiums can exceed $500–$1,000 per month for families.

-

-

Government Health Insurance:

-

Funded primarily by taxes, making it more affordable or even free at the point of service.

-

Premiums (if applicable) are usually lower.

-

Out-of-pocket expenses are minimized.

-

Example: Medicaid in the U.S. or NHS in the UK covers most essential healthcare at little to no cost.

-

Verdict: Government plans are more budget-friendly, but private plans offer more flexibility and additional services at higher costs.

Coverage and Benefits

Coverage is another crucial factor when comparing both types of insurance.

Private Health Insurance:

-

Covers a wide range of services, including elective surgeries, advanced diagnostic tests, and specialized treatments.

-

Offers dental, vision, maternity, and wellness program add-ons.

-

Provides better coverage for international healthcare services in some cases.

Government Health Insurance:

-

Focuses primarily on essential healthcare needs: emergency care, preventive services, and chronic disease management.

-

May not cover non-essential services like cosmetic surgery, extensive dental or vision care.

-

Sometimes limited to in-network government hospitals and clinics.

Verdict: Private plans offer broader and more comprehensive coverage, while government plans focus on basic, essential care.

Accessibility and Waiting Times

Private Health Insurance:

-

Patients enjoy quicker access to elective surgeries, diagnostic tests, and specialist consultations.

-

Reduced waiting times because of broader healthcare provider availability.

Government Health Insurance:

-

Longer waiting times, particularly in systems with universal healthcare where demand is high.

-

Emergency cases are prioritized, but elective procedures may be delayed for weeks or months.

Verdict: Private insurance offers speed and convenience, while government insurance may involve delays.

Provider Network and Choice

Private Insurance:

-

Greater choice of hospitals, doctors, and specialists.

-

Some plans allow out-of-network care with partial reimbursement.

Government Insurance:

-

Restricted to government hospitals and approved providers.

-

Limited flexibility in choosing doctors and specialists.

Verdict: Private insurance provides freedom of choice, whereas government insurance limits provider selection.

Quality of Care

Private Health Insurance:

-

Access to modern facilities, private hospital rooms, and advanced medical technology.

-

Higher doctor-to-patient ratios.

-

Perceived as offering “premium” healthcare experiences.

Government Health Insurance:

-

Provides standard medical care but often faces issues like overcrowded hospitals, outdated equipment, and stretched resources.

-

Quality can vary depending on the country and funding levels.

Verdict: Quality tends to be higher in private healthcare facilities, but government care ensures essential services for all.

Eligibility Criteria

Private Health Insurance:

-

Available to anyone who can afford it.

-

Premiums may be higher for older adults or people with pre-existing conditions.

Government Health Insurance:

-

Eligibility is often based on income level, age, disability, or employment status.

-

Universal healthcare systems cover all residents, regardless of status.

Verdict: Private insurance is universally available (at a cost), while government insurance depends on eligibility rules.

Pros and Cons of Private Health Insurance

Pros:

-

Faster access to care

-

Wide provider networks

-

Comprehensive coverage options

-

More privacy and comfort in hospitals

Cons:

-

Expensive premiums and out-of-pocket costs

-

Can exclude pre-existing conditions

-

Not affordable for everyone

Pros and Cons of Government Health Insurance

Pros:

-

Affordable or free coverage

-

Ensures healthcare access for vulnerable populations

-

Reduces financial burden during emergencies

-

Promotes equity in healthcare

Cons:

-

Limited coverage for non-essential services

-

Long waiting times

-

Restricted provider choice

-

Quality may vary depending on resources

Which One Should You Choose?

The decision depends on personal circumstances, budget, and healthcare needs:

-

Choose Private Health Insurance If:

-

You want faster access to care.

-

You need specialized or elective procedures.

-

You prefer private hospital facilities and broader provider choices.

-

You can afford higher premiums.

-

-

Choose Government Health Insurance If:

-

You want affordable or free essential healthcare.

-

You qualify based on income, age, or residency.

-

You don’t mind longer waiting times for non-urgent care.

-

You want basic but reliable medical coverage.

-

The Global Perspective

The balance between private and government health insurance varies across countries:

-

United States: A mixed system with Medicare, Medicaid, and private insurance dominating.

-

United Kingdom: Primarily government-funded (NHS), with private insurance as a supplement.

-

Canada: Universal healthcare system with private insurance available for non-covered services.

-

Pakistan/India: Limited government coverage, with private insurance or out-of-pocket payments playing a significant role.

Future of Health Insurance

The future may see more hybrid systems, where private and government insurance work together. Governments may continue expanding universal coverage, while private insurers may offer supplementary services like dental, vision, and faster access to care. Technology, telemedicine, and health data analytics will also influence the evolution of both systems.

Conclusion

The difference between private and government health insurance plans lies in cost, coverage, accessibility, provider choice, and quality of care. While government health insurance ensures affordable access to essential healthcare, private health insurance provides faster, more comprehensive, and customizable options—albeit at a higher cost.

The right choice depends on your financial situation, healthcare priorities, and eligibility. For many people, a combination of both systems—using government insurance for basic coverage and private insurance for additional services—offers the best balance of affordability and quality.