Health insurance is one of the most important financial tools you can have to protect yourself and your family from unexpected medical expenses. However, health insurance policies often contain terms and structures that can be confusing for beginners. Two of the most critical concepts to grasp are premiums and deductibles. Together, they determine how much you pay for your health insurance and how much coverage you receive when medical care is needed.

This article provides a comprehensive breakdown of health insurance premiums and deductibles, how they work, their differences, and practical tips for choosing the right balance for your situation.

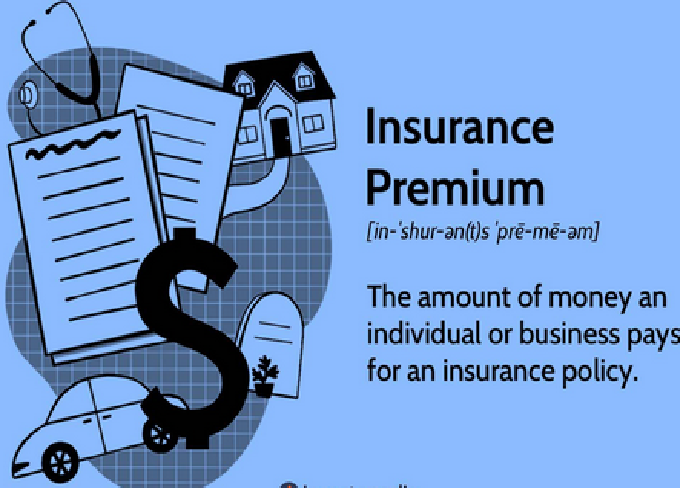

What Is a Health Insurance Premium?

A health insurance premium is the amount of money you pay to your insurance provider to maintain your coverage. It is typically billed monthly, although some insurers may offer quarterly or annual payment options.

Think of it as a subscription fee for your health insurance plan. Whether you use medical services or not, you must pay your premium to keep your insurance active.

Key Points About Premiums:

-

Paid regularly (monthly, quarterly, or annually).

-

Required to maintain coverage.

-

Premiums vary depending on the type of plan, coverage, age, location, and health status (in some countries).

-

Lower premiums often come with higher deductibles, while higher premiums may reduce out-of-pocket costs.

Factors That Affect Health Insurance Premiums

Insurance companies calculate premiums based on several factors. Understanding these can help you predict costs and compare plans more effectively.

1. Age

Generally, the older you are, the higher your premiums will be. This is because older individuals are statistically more likely to require medical care.

2. Location

Healthcare costs vary by region, and so do insurance premiums. Living in an area with high medical service costs often leads to higher premiums.

3. Coverage Level

Plans with comprehensive coverage (including dental, vision, maternity, etc.) cost more than basic coverage plans.

4. Type of Plan

Different plans such as HMO (Health Maintenance Organization), PPO (Preferred Provider Organization), or catastrophic plans come with varying premium levels.

5. Family Size

Insuring a family is more expensive than an individual plan, though family plans may be more affordable per person.

6. Lifestyle and Health

In some countries, smoking, obesity, or pre-existing conditions can lead to higher premiums. However, in regulated markets like the United States under the Affordable Care Act, insurers cannot charge more based on certain health conditions.

What Is a Deductible in Health Insurance?

A deductible is the amount you must pay out of your own pocket for healthcare services before your insurance company starts covering costs.

For example, if your deductible is $1,500, you will have to pay the first $1,500 of covered medical expenses yourself before your insurance coverage kicks in.

Key Points About Deductibles:

-

It is an annual amount, resetting every year.

-

You must meet your deductible before insurance covers most services (exceptions may apply, such as preventive care).

-

Plans with lower premiums often have higher deductibles.

-

After meeting the deductible, you usually share costs with the insurer through copayments or coinsurance.

How Deductibles Work in Practice

Imagine you have a health insurance plan with the following terms:

-

Monthly premium: $300

-

Deductible: $2,000

-

Coinsurance: 20% (you pay 20% after meeting deductible)

-

Out-of-pocket maximum: $6,000

If you visit the hospital for a treatment costing $5,000:

-

You first pay the $2,000 deductible.

-

The remaining $3,000 is shared under coinsurance. You pay 20% ($600), and the insurer pays 80% ($2,400).

-

In total, you pay $2,600 out of pocket.

This example highlights why understanding deductibles is crucial before choosing a plan.

The Relationship Between Premiums and Deductibles

Premiums and deductibles are interconnected. When one goes up, the other usually goes down.

-

Low Premium, High Deductible Plans

-

Best for healthy individuals who rarely need medical care.

-

Lower monthly cost but higher risk if unexpected medical bills arise.

-

-

High Premium, Low Deductible Plans

-

Best for individuals with chronic conditions or frequent medical needs.

-

Higher monthly cost but lower financial burden when receiving treatment.

-

Common Types of Deductibles

Not all deductibles are the same. Here are the most common types:

1. Individual vs. Family Deductibles

-

Individual Deductible: Applies to each covered person separately.

-

Family Deductible: Once the family as a whole meets the deductible, insurance covers everyone, even if some members didn’t meet their individual portion.

2. Embedded vs. Non-Embedded Deductibles

-

Embedded Deductible: Each family member has an individual deductible within the family plan.

-

Non-Embedded Deductible: Only the total family deductible matters.

3. Prescription Drug Deductibles

Some plans have a separate deductible specifically for medications.

4. Specialty Deductibles

Certain services (like maternity or mental health care) may have their own deductible requirements.

Out-of-Pocket Maximum and Its Role

The out-of-pocket maximum is the total amount you will pay in a year for covered services, including deductibles, copays, and coinsurance. Once you reach this limit, your insurance covers 100% of eligible expenses for the rest of the year.

This protects you from catastrophic healthcare costs.

Examples to Compare Plans

Let’s compare two health insurance plans to illustrate how premiums and deductibles affect total costs.

Plan A:

-

Premium: $250/month ($3,000 annually)

-

Deductible: $5,000

-

Out-of-pocket maximum: $7,500

Plan B:

-

Premium: $500/month ($6,000 annually)

-

Deductible: $1,000

-

Out-of-pocket maximum: $3,500

If you stay healthy all year:

-

Plan A costs $3,000 (just premiums).

-

Plan B costs $6,000.

Plan A is cheaper for healthy individuals.

If you have a $10,000 surgery:

-

Under Plan A: You pay $5,000 deductible + part of coinsurance, possibly reaching $7,500.

-

Under Plan B: You pay $1,000 deductible + coinsurance, capped at $3,500.

Plan B is cheaper if you need expensive care.

Pros and Cons of Low vs. High Deductible Plans

Low Deductible (High Premium)

✅ Predictable costs

✅ Better for frequent healthcare needs

❌ Expensive monthly payments

High Deductible (Low Premium)

✅ Affordable monthly payments

✅ Good for healthy, young adults

❌ Risk of high medical bills if unexpected illness occurs

How to Choose the Right Balance

Choosing between high premiums with low deductibles or low premiums with high deductibles depends on your personal situation.

Consider:

-

Your Health Status

-

If you have ongoing health issues, a low deductible may be better.

-

If you are young and healthy, a high deductible plan may save money.

-

-

Your Budget

-

Can you afford high monthly premiums consistently?

-

Do you have savings to cover a high deductible if needed?

-

-

Frequency of Medical Visits

-

Frequent doctor visits justify a low deductible.

-

Rare medical use supports a high deductible.

-

-

Risk Tolerance

-

Are you comfortable with financial uncertainty?

-

Do you prefer stable, predictable costs?

-

Tips for Managing Premiums and Deductibles

-

Use Preventive Services: Many plans cover preventive care at no extra cost, even before meeting your deductible.

-

Consider Health Savings Accounts (HSAs): Available with high-deductible plans, HSAs let you save pre-tax money for medical expenses.

-

Shop Around Annually: Compare plans each year during open enrollment to ensure you’re not overpaying.

-

Estimate Expected Costs: If you expect major healthcare needs, calculate which plan saves more overall.

-

Employer-Sponsored Plans: If offered, these often provide better premium and deductible balances.

Common Misconceptions

Misconception 1: “Low Premiums Always Save Money”

Not true—if you end up needing care, high deductibles may cost more overall.

Misconception 2: “Once I Pay My Premium, Insurance Covers Everything”

Premiums keep your policy active, but deductibles, copays, and coinsurance still apply.

Misconception 3: “Preventive Care Requires Meeting the Deductible First”

In most modern plans, preventive services like vaccinations and screenings are covered even before deductibles.

The Global Perspective

Premiums and deductibles are structured differently around the world:

-

United States: Premiums and deductibles play a central role in health insurance under private and employer-sponsored systems.

-

Europe: Many countries use public insurance, where deductibles are minimal or non-existent.

-

Asia: Countries like Singapore use medical savings accounts alongside insurance, while others rely on government-funded healthcare.

Future Trends in Premiums and Deductibles

Healthcare costs continue to rise worldwide, which affects both premiums and deductibles. Some trends include:

-

Growth of high-deductible health plans (HDHPs).

-

Increased use of telemedicine to reduce costs.

-

Expansion of value-based care, where insurers focus on outcomes rather than service quantity.

-

Government regulations aiming to limit excessive out-of-pocket costs.

Conclusion

Health insurance premiums and deductibles are the foundation of how insurance policies work. Premiums represent the cost of maintaining coverage, while deductibles determine how much you pay before insurance helps with medical expenses.

The balance between the two directly affects your financial security and peace of mind. High-deductible plans may save money for healthy individuals, while low-deductible plans provide stability for those with frequent medical needs.

By carefully analyzing your health, budget, and risk tolerance, you can select the plan that offers the best protection without overspending. Ultimately, understanding premiums and deductibles empowers you to make smarter healthcare decisions and avoid financial strain in times of medical need.