Owning a vehicle is more than just a convenience—it’s a responsibility. Driving brings freedom, but it also comes with risks, from accidents and theft to unexpected natural disasters. This is where auto insurance steps in as a safeguard. For many drivers, auto insurance is often seen as just another financial burden, but in reality, it’s one of the most essential protections you can have on the road.

In this comprehensive guide, we’ll explore why every driver needs auto insurance, what it covers, how it works, the different types of policies available, and how to choose the best one for your needs.

1. Understanding Auto Insurance

What Is Auto Insurance?

Auto insurance is a contract between you and an insurance company. In exchange for regular premium payments, the insurer provides financial protection against losses related to your vehicle. These losses may include accidents, theft, natural disasters, or damages caused to others.

Why It Matters

Accidents are unpredictable. Even the most careful driver can face unforeseen situations on the road. Auto insurance ensures that drivers don’t face massive financial setbacks when these events occur.

2. Legal Requirement: It’s Not Optional in Most Places

Mandatory Coverage by Law

In many countries and states, carrying at least a minimum level of auto insurance is legally required. Driving without insurance can result in fines, license suspension, or even jail time.

Protecting All Road Users

Mandatory insurance laws exist to protect not just the driver but also passengers, pedestrians, and other motorists. Without insurance, victims of accidents could be left uncompensated, leading to legal disputes and financial hardship.

3. Financial Protection Against Accidents

Covering Repair Costs

Car accidents can be expensive. Even a minor fender-bender could result in repair bills that run into thousands of dollars. Auto insurance helps cover these costs, reducing the financial burden.

Medical Expenses

Beyond property damage, injuries can be even more costly. Hospital bills, rehabilitation, and long-term care can drain savings quickly. With the right coverage, medical costs are handled by the insurer.

Protecting Against Lawsuits

If you’re found at fault in an accident, the injured party could sue you. Liability insurance covers legal fees, settlements, and damages, saving you from financial ruin.

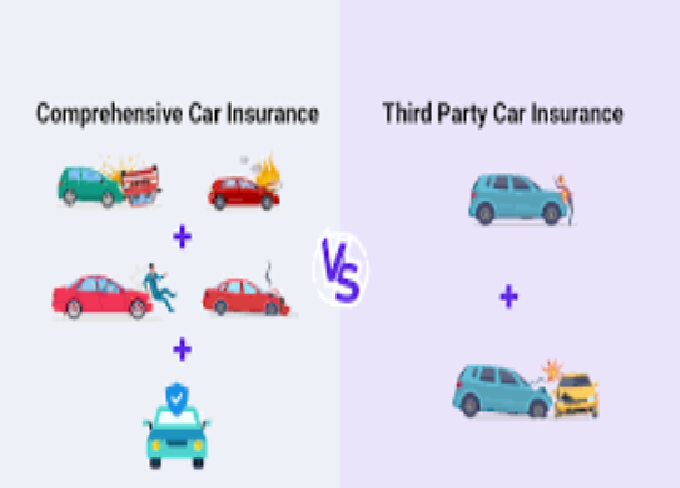

4. Types of Auto Insurance Coverage

a) Liability Insurance

This is the most basic coverage and is often legally required. It pays for damages and injuries you cause to others in an accident.

b) Collision Coverage

Covers damages to your own vehicle in case of a collision with another car or object, regardless of who is at fault.

c) Comprehensive Coverage

Protects your car against non-collision events like theft, fire, natural disasters, vandalism, or falling objects.

d) Personal Injury Protection (PIP)

Covers medical expenses for you and your passengers, regardless of fault. In some places, it also compensates for lost wages.

e) Uninsured/Underinsured Motorist Coverage

Protects you if you’re hit by a driver who has no insurance or insufficient coverage to pay for damages.

f) Optional Add-Ons

-

Roadside assistance

-

Rental car reimbursement

-

Gap insurance (for new cars with outstanding loans)

5. Real-Life Scenarios Where Auto Insurance Saves You

Accident Example

Imagine causing a multi-car pile-up. Without insurance, you’d face not only your repair bills but also liability for all other damaged vehicles and medical costs. Insurance absorbs most of this financial shock.

Theft Example

If your car gets stolen, comprehensive insurance helps you replace it, saving you from total loss.

Natural Disaster Example

A flood or hailstorm damages your vehicle. Without coverage, you pay from pocket. With comprehensive insurance, your insurer covers the loss.

6. Peace of Mind: Driving Without Worry

One of the less-discussed benefits of auto insurance is the psychological relief it provides. Knowing you’re protected against unforeseen events allows you to focus on driving safely instead of constantly worrying about “what if something happens.”

7. Auto Insurance vs. Out-of-Pocket Costs

The Cost of an Accident Without Insurance

-

Minor accident repair: $2,000–$5,000

-

Serious accident repairs: $10,000+

-

Hospital bills: $50,000–$100,000

-

Legal settlements: Potentially millions

The Cost of Auto Insurance

On average, monthly premiums range between $50 and $200, depending on location, driving record, and coverage type. Clearly, insurance is far cheaper than facing accident costs alone.

8. Factors That Affect Auto Insurance Premiums

Driving History

Accidents, speeding tickets, or DUI charges can significantly increase premiums.

Type of Vehicle

Luxury cars, sports cars, or vehicles with expensive parts cost more to insure.

Age and Gender

Young drivers typically pay higher premiums due to inexperience.

Location

Urban areas with higher traffic or crime rates usually have higher premiums.

Coverage Level

The more comprehensive the policy, the higher the premium.

9. Common Myths About Auto Insurance

“Red Cars Cost More to Insure”

False. The color of your car has no impact on premiums.

“Older Drivers Always Pay Less”

Not always. While experience can reduce premiums, health issues or accident history may increase them.

“Minimum Coverage Is Enough”

Minimum legal coverage may not protect you adequately in serious accidents. Comprehensive coverage is often a smarter choice.

10. Choosing the Right Auto Insurance Policy

Assess Your Needs

Consider your car’s value, your driving habits, and your budget.

Compare Policies

Don’t settle for the first offer. Compare coverage options, premiums, and customer service ratings.

Read the Fine Print

Understand exclusions, deductibles, and claim procedures before signing.

Seek Discounts

Look for safe driver discounts, bundling with home insurance, or loyalty rewards.

11. The Claims Process: How It Works

Step 1: Report the Incident

Notify your insurer immediately after an accident or damage.

Step 2: Provide Documentation

Submit police reports, photos, and repair estimates.

Step 3: Assessment

An adjuster evaluates the damage and determines compensation.

Step 4: Settlement

The insurer pays for repairs, medical bills, or liability claims as per policy terms.

12. Global Perspective: Auto Insurance Across Countries

United States

Most states mandate liability insurance, but coverage levels vary.

Europe

Countries like the UK require third-party insurance, while others encourage comprehensive coverage.

Asia

In countries like India and Pakistan, third-party liability insurance is mandatory, with comprehensive policies as optional add-ons.

Middle East

Insurance laws differ, but in most Gulf countries, third-party liability is mandatory.

13. The Future of Auto Insurance

Telematics and Usage-Based Insurance

Insurers now use GPS and driving behavior data to set premiums. Safe drivers pay less.

Electric and Autonomous Cars

New vehicle technology will influence insurance needs, premiums, and policies in the future.

On-Demand Insurance

With ride-sharing and occasional driving, flexible, pay-per-mile insurance is gaining popularity.

14. Benefits of Auto Insurance Beyond Coverage

-

Legal protection in case of lawsuits.

-

Financial security during uncertain times.

-

Access to roadside assistance for emergencies.

-

Support services like towing, rental cars, and repairs.

-

Improved creditworthiness as insurers share responsible payment history with credit agencies.

15. Conclusion: Why Auto Insurance Is Non-Negotiable

Auto insurance is more than a legal formality; it’s a shield against financial disaster, a protector of health, and a provider of peace of mind. Whether it’s covering accident costs, protecting you from lawsuits, or ensuring you don’t lose your vehicle to theft or natural disasters, insurance is an indispensable tool for every driver.

The reality is simple: driving without insurance is like walking a tightrope without a safety net. For a relatively small investment, you gain security, stability, and confidence on the road.

So, the next time you think about skipping or reducing your auto insurance coverage, remember—it’s not just about protecting your car; it’s about protecting your life, your finances, and your future.