Auto accidents happen every day, ranging from minor fender-benders to serious collisions that cause significant injuries and property damage. When such incidents occur, auto insurance plays a critical role in protecting drivers, passengers, and even pedestrians from devastating financial losses. Accident claims can be confusing and overwhelming, especially when you’re unsure how insurance companies assess damages, handle medical costs, and manage liability. This article provides a comprehensive breakdown of the role of auto insurance in accident claims, helping you understand the process, the coverage types, and what you should expect after a collision.

Understanding Auto Insurance Basics

Before diving into accident claims, it’s essential to understand what auto insurance is and why it exists.

-

Definition: Auto insurance is a contract between a driver and an insurance company. The driver pays a premium, and in exchange, the insurer promises to cover specific types of losses resulting from accidents, theft, or other vehicle-related damages.

-

Primary Purpose: It serves as a financial safety net. Without insurance, individuals would have to pay out of pocket for repairs, medical bills, or lawsuits arising from an accident.

-

Legal Requirement: In most countries and states, auto insurance is mandatory. Drivers must carry at least minimum liability coverage to legally operate a vehicle.

Insurance ensures that victims of accidents are not left uncompensated and that at-fault drivers can fulfill their financial responsibilities.

Types of Auto Insurance Coverage Relevant to Accident Claims

Different types of coverage come into play during an accident claim. Understanding these will help you see how they apply in various situations.

-

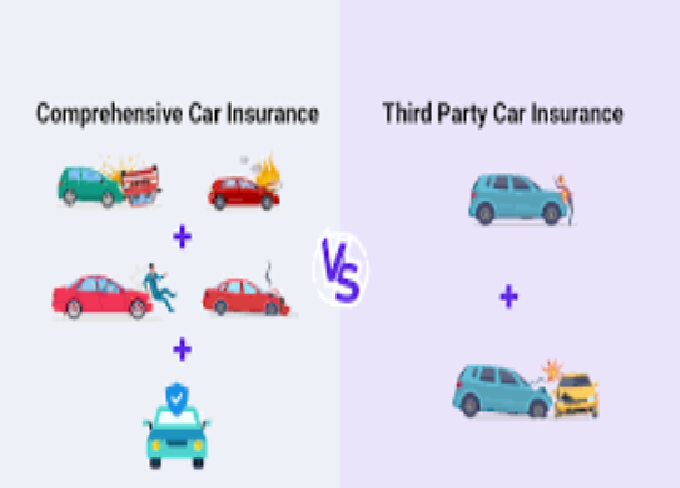

Liability Insurance

-

Covers injuries and property damage caused to others if you’re at fault.

-

Does not cover your own injuries or vehicle repairs.

-

It’s often divided into bodily injury liability and property damage liability.

-

-

Collision Coverage

-

Pays for the repair or replacement of your car if it’s damaged in a crash, regardless of fault.

-

Particularly useful if the other driver is uninsured or underinsured.

-

-

Comprehensive Coverage

-

Covers non-collision-related damages, such as theft, fire, vandalism, or natural disasters.

-

May apply if your car is totaled after an accident.

-

-

Personal Injury Protection (PIP)

-

Covers medical expenses for you and your passengers.

-

In some regions, it also provides coverage for lost wages and rehabilitation.

-

-

Uninsured/Underinsured Motorist Coverage

-

Protects you if you’re hit by a driver with little or no insurance.

-

Essential because not everyone follows insurance requirements.

-

-

Medical Payments Coverage (MedPay)

-

Similar to PIP but usually limited to medical expenses only.

-

Each of these coverage types can affect how an accident claim unfolds.

The Role of Auto Insurance Immediately After an Accident

After an accident, your insurance policy determines how financial responsibility is allocated. Here’s what typically happens:

-

Accident Reporting

-

Drivers are usually required to report an accident to their insurance provider as soon as possible.

-

Prompt reporting ensures faster processing and avoids disputes.

-

-

Claim Filing

-

You’ll file a claim with your insurance company (or the other driver’s, depending on fault).

-

Claims typically require details such as accident date, location, parties involved, and police reports.

-

-

Initial Coverage

-

Insurance may provide immediate help, such as covering a rental car, towing, or medical treatment advances.

-

This early stage sets the foundation for the claim process.

The Investigation and Assessment Process

Insurance companies don’t simply take your word for what happened—they investigate thoroughly. Here’s how:

-

Claim Adjuster Assignment

-

An insurance adjuster is assigned to your case.

-

Their role is to assess damages, verify facts, and determine liability.

-

-

Evidence Collection

-

Adjusters collect police reports, witness statements, photos, and even traffic camera footage.

-

They may inspect vehicles and consult medical records.

-

-

Fault Determination

-

Fault can be clear-cut (e.g., rear-end collision) or complicated (multi-car pileups).

-

In some regions, fault is shared under comparative negligence laws.

-

-

Damage Estimation

-

Adjusters estimate vehicle repair costs and medical expenses.

-

They may consult with mechanics, doctors, and accident reconstruction specialists.

-

This stage is critical because it directly impacts the settlement you receive.

How Auto Insurance Handles Property Damage Claims

When a car is damaged, insurance ensures repairs or replacement costs are covered according to policy terms.

-

Repair vs. Replacement

-

If the car can be repaired economically, insurance pays for parts and labor.

-

If the car is a “total loss” (repair costs exceed the car’s value), the insurer pays the actual cash value (ACV).

-

-

Deductibles

-

Drivers must often pay a deductible before insurance kicks in.

-

Example: If you have a $500 deductible and $2,500 in damages, you pay $500, and insurance covers $2,000.

-

-

Third-Party Claims

-

If another driver was at fault, their liability insurance pays for your property damage.

-

If they lack coverage, your collision or uninsured motorist policy may step in.

-

This ensures you’re not left stranded with repair bills.

How Auto Insurance Handles Injury Claims

Injury claims are often the most complicated part of accident cases. Auto insurance plays a key role in ensuring medical costs are addressed fairly.

-

Immediate Medical Bills

-

PIP or MedPay coverage can pay hospital expenses right away.

-

This prevents victims from delaying treatment.

-

-

Ongoing Care and Rehabilitation

-

Insurance can cover follow-up treatments, physical therapy, and long-term rehabilitation.

-

-

Lost Income Compensation

-

PIP often covers a portion of lost wages if injuries prevent you from working.

-

-

Pain and Suffering

-

In some cases, victims can claim compensation for non-economic damages such as emotional distress.

-

Typically falls under bodily injury liability.

-

-

Liability Coverage for Others

-

If you caused the accident, your liability insurance pays the injured party’s medical bills and related expenses.

-

This system ensures victims aren’t left without recourse.

The Role of Insurance in Legal Disputes

Not all accident claims are settled quickly or amicably. Sometimes, disputes arise:

-

Disagreement on Fault

-

If both drivers claim innocence, insurers may argue over liability.

-

-

Disagreement on Settlement Amounts

-

Victims may feel offered settlements are too low.

-

-

Lawsuits

-

When negotiations fail, lawsuits may follow. Insurance companies often provide legal defense for their policyholders.

-

Auto insurance doesn’t just pay claims; it also shields drivers from crushing legal expenses.

Comparative and Contributory Negligence in Claims

Fault laws vary depending on where you live, and insurance companies use them to calculate claim payouts.

-

Comparative Negligence

-

Damages are divided based on each driver’s percentage of fault.

-

Example: If you’re 30% at fault, you can only recover 70% of damages.

-

-

Contributory Negligence

-

If you’re even 1% at fault, you may not recover any damages.

-

Stricter and less favorable to accident victims.

-

Understanding your state or country’s negligence system is crucial to knowing what insurance will cover.

The Impact of Accident Claims on Insurance Premiums

Filing an accident claim often affects your future premiums. Insurance companies view claims as indicators of risk.

-

At-Fault Claims

-

If you caused the accident, expect your premiums to rise significantly.

-

-

Not-at-Fault Claims

-

Premiums may still increase slightly, as insurers see you as a higher-risk driver.

-

-

Claim Frequency

-

Multiple claims within a short period can result in much higher premiums or even policy cancellation.

-

Some insurers offer accident forgiveness programs, where your first claim won’t raise rates.

The Role of Auto Insurance in Hit-and-Run Accidents

Hit-and-run cases are especially challenging since the at-fault driver is unidentified. Insurance becomes the primary source of protection:

-

Uninsured Motorist Coverage often applies, covering damages as if the other driver had no insurance.

-

Collision Coverage can pay for your car repairs, even without identifying the other driver.

-

Medical Payments Coverage can handle injury expenses.

Without proper insurance, victims of hit-and-runs could face heavy financial burdens.

Steps to Strengthen Your Accident Claim

Insurance companies rely heavily on evidence and documentation. You can improve your claim by:

-

Collecting Evidence

-

Take photos of the accident scene, damages, and injuries.

-

Get witness statements and contact details.

-

-

Obtaining a Police Report

-

A police report is a powerful piece of evidence when determining fault.

-

-

Seeking Immediate Medical Care

-

Even minor injuries should be documented by a doctor.

-

-

Keeping All Records

-

Save receipts for repairs, medical bills, and related expenses.

-

-

Avoiding Admitting Fault

-

Leave fault determination to the insurance companies and authorities.

-

These steps increase the chances of a fair settlement.

Common Challenges in Accident Claims

While insurance is meant to protect you, the claim process can be frustrating. Common issues include:

-

Delays in Processing

-

Claims can take weeks or months if investigations are complex.

-

-

Lowball Settlements

-

Insurance companies may offer less than what you deserve.

-

-

Policy Exclusions

-

Some damages may not be covered due to specific policy terms.

-

-

Disputes Over Coverage

-

Insurers may argue whether certain damages fall under your policy.

-

Being prepared and informed helps you avoid these pitfalls.

The Importance of Legal Assistance in Claims

While many claims are resolved smoothly, some require professional help. Accident victims often benefit from consulting a lawyer when:

-

Injuries are severe and long-term.

-

There is a dispute over fault.

-

The insurer denies a valid claim.

-

Settlement offers are inadequate.

Lawyers understand insurance laws, negotiation tactics, and court procedures, ensuring you get the compensation you deserve.

Future of Auto Insurance in Accident Claims

Technology is transforming how accident claims are handled:

-

Telematics and Dashcams: Many insurers now use driving data and dashcam footage to verify claims.

-

AI in Claims Processing: Artificial intelligence speeds up settlement decisions.

-

Blockchain Records: May prevent fraud by providing tamper-proof accident histories.

-

Autonomous Vehicles: As self-driving cars become common, liability rules and insurance claims will evolve dramatically.

The insurance industry is adapting to make accident claims more efficient and fair.

Conclusion

Auto insurance is the backbone of accident claims, ensuring victims receive compensation and at-fault drivers can fulfill their responsibilities. From covering property damage and medical bills to handling lawsuits and hit-and-run cases, insurance plays a vital role in minimizing the financial impact of accidents. While the claim process can be challenging, understanding how it works—and what steps you should take—empowers you to protect your rights and recover fully.

As vehicles and technology evolve, so will the landscape of auto insurance. But its core purpose remains unchanged: providing peace of mind and financial protection when accidents happen.