Choosing the right car insurance can feel like decoding a foreign language while juggling a steering wheel. Two of the most common options are Comprehensive (sometimes bundled with collision) and Third-Party auto insurance. They sound similar but protect you very differently. This article breaks both down in detail — what each covers, how premiums are calculated, real-world examples, advantages and drawbacks, legal considerations, add-ons to consider, and a practical decision framework so you can make an informed choice.

What each policy actually means

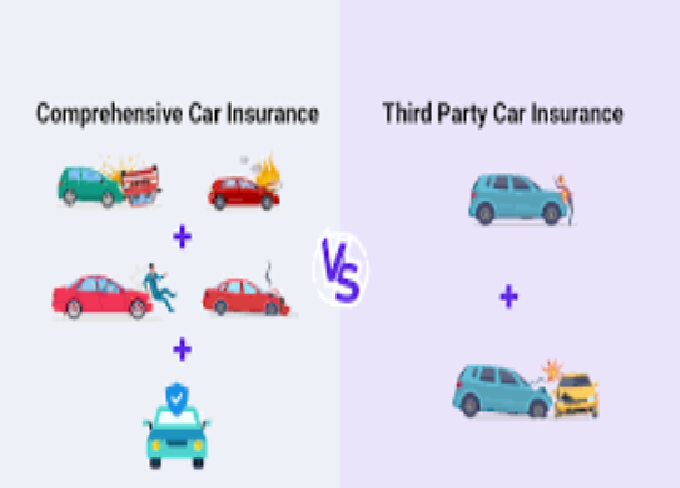

Third-Party Auto Insurance (also called Third-Party Liability)

Third-party insurance primarily covers damage or injury you cause to other people or their property. If you’re at fault in an accident, this policy pays for:

-

Repairs to the other vehicle(s)

-

Property damage (fences, poles, buildings)

-

Medical costs of injured third parties

-

Legal liabilities and court/settlement costs if you’re sued

What it does NOT cover: damage to your own vehicle, theft of your vehicle, vandalism to your vehicle, or damages from natural events (flood, fire, hail) to your own vehicle.

Comprehensive Auto Insurance

Comprehensive is a wider form of protection that often includes third-party liability plus cover for many risks to your own vehicle that are not collision with another vehicle. Typical coverage includes:

-

Theft of your vehicle

-

Vandalism

-

Fire and explosions

-

Natural disasters (storm, flood, hail, earthquake — depending on policy)

-

Falling objects (trees, debris)

-

Animal collisions (hitting a deer, etc.)

-

Broken glass, windscreen repairs

Comprehensive is frequently packaged with collision coverage (which pays for damage to your vehicle after a crash, regardless of fault) and liability — together these create an “all-risk” motor insurance policy in many markets.

Who needs which — quick summary

-

Choose Third-Party if: you drive an older low-value car, are on a tight budget, or you live somewhere where comprehensive is prohibitively expensive or unnecessary.

-

Choose Comprehensive if: you have a newer/expensive car, rely heavily on the vehicle, live in an area with high theft or natural disaster risk, or prefer peace of mind for repair/replace costs.

Cost comparison: premiums, deductibles, and value

Premiums

-

Third-party premiums are typically much lower because insurers aren’t taking on the risk of repairing/replacing your vehicle.

-

Comprehensive premiums are higher because the insurer covers a wider set of risks — including theft, fire, and sometimes collision.

Deductibles

Comprehensive policies usually include a deductible (the amount you pay before the insurer pays the rest). Choosing a higher deductible lowers your premium but increases your out-of-pocket cost when you claim.

Third-party policies generally don’t involve a deductible for the other party’s claim (you’re not claiming on your own vehicle), though some markets might have specific rules or optional add-ons with deductibles.

Value for money

-

If repairing or replacing your car would be a serious financial burden, comprehensive is often worth the higher premium.

-

If your vehicle’s market value is low (older, depreciated), paying high comprehensive premiums may make less sense — you might pay more in premiums over a few years than you’d ever get back on a claim.

What’s covered — concrete examples

Third-Party scenarios (what you’re protected against)

-

You run a red light and hit a car. The other driver is injured and their car is totaled. Third-party insurance pays their medical bills and car repair/replace costs — you’re protected from their claims.

-

You clip a parked car while reversing; the owner sues for damages. Your third-party liability helps cover that.

Comprehensive scenarios (what it adds)

-

A thief takes your car overnight and it’s not recovered: comprehensive typically pays the vehicle’s market value (minus deductible).

-

A hailstorm shatters your windscreen: comprehensive covers glass repair or replacement.

-

You hit a deer on a rural road and damage your bumper: comprehensive (or collision, if included) covers repairs.

-

Your car is damaged in a city riot or by vandalism: comprehensive covers it.

Note: Collision is the standard add-on for accident damage to your own car; some comprehensive packages include collision, others separate it. Always check the policy wording.

Pros & cons, side by side

Third-Party Insurance

Pros

-

Lowest cost

-

Meets minimum legal requirements in many countries

-

Good for low-value cars or if you don’t mind covering your own repairs

Cons

-

No protection for theft, fire, or damage to your own vehicle

-

If you’re hit by an uninsured driver and can’t recover damages, you bear the cost

-

May leave you significantly out of pocket after a serious loss

Comprehensive Insurance

Pros

-

Broad protection — covers own damage, theft, natural disasters, vandalism

-

Greater financial security and peace of mind

-

Often includes extras (windshield repair, towing, roadside assistance) depending on insurer

Cons

-

Higher premiums

-

May have exclusions/limits and deductibles

-

Might be less cost-effective for very old/low-value cars

Legal and market considerations

-

In many countries, third-party liability is the legal minimum. You may be required to hold at least third-party cover to drive.

-

Comprehensive is optional but sometimes required by lenders — if your car is financed or leased, the bank may demand comprehensive coverage.

-

Policy wording matters: coverage definitions, exclusions (e.g., war, deliberate damage, unauthorized drivers), and claim procedures vary by insurer and jurisdiction. Read the policy schedule and wording carefully.

How insurers calculate premiums (factors that matter)

-

Car make, model, and age: expensive or high-performance cars cost more to insure.

-

Vehicle value: higher replacement cost → higher premium.

-

Driver age and driving history: young or risky drivers pay more.

-

Location: areas with high theft, vandalism, or accident rates raise premiums.

-

Usage: business vs personal use, annual kilometers driven.

-

Security features: immobilizers, tracking devices, secure parking may reduce premium.

-

No-claim bonus (NCB): years without claims can discount premium substantially.

-

Claims history: prior claims make premiums higher.

-

Deductible chosen: higher deductible reduces premium.

Add-ons and optional extras to consider

Whether you choose third-party or comprehensive, insurers often offer add-ons that enhance protection:

-

Zero Depreciation Cover: insurer pays full parts cost without depreciation deduction (useful for newer cars).

-

Roadside Assistance / Towing: helpful for breakdowns or accidents.

-

Windshield / Glass Cover: covers glass repairs without affecting NCB in some policies.

-

Engine & Gearbox Protection: covers mechanical failures due to water ingress or other incidents (be wary of exclusions).

-

Personal Accident Cover: extra payout for driver/passenger bodily injury or death.

-

Legal Expense Cover: pays for legal costs arising from disputes.

-

Return to Invoice / GAP Cover: for totaled vehicles, pays difference between insurer payout and original invoice/loan amount — valuable for new cars under finance.

Add-ons raise premiums but can be cost-effective if the risk they cover is meaningful to you.

Claim process — what to expect

Third-Party claim

-

Exchange details and report accident.

-

File a claim with your insurer (or with the third party’s insurer).

-

Insurer investigates fault and pays the third party’s losses if you’re liable.

-

There is no payout to you for vehicle repairs under third-party.

Comprehensive claim

-

Report the loss ASAP to your insurer and police if required (theft, vandalism, major accident).

-

Provide documents: policy, driving license, registration, FIR/police report (if applicable), photos.

-

Insurer appoints surveyor to assess damage.

-

Pay the deductible; insurer arranges repair or pays cash settlement (market value).

-

Your no-claim bonus may be affected depending on terms and whether you paid for protection.

Real-world decision framework — simple checklist

Ask yourself:

-

How old and valuable is my car? If older and worth little, third-party may be logical.

-

How much can I afford to pay out of pocket to repair/replace? If a total loss would be devastating, comprehensive is safer.

-

Do I have a loan/lease? If yes, lender likely requires comprehensive.

-

Where I park and drive: high-crime or flood-prone areas favor comprehensive.

-

How often do I drive? Daily drivers face higher exposure than occasional users.

-

What’s my risk tolerance? Some people accept the gamble of third-party to save monthly money; others prefer certainty.

-

Do I value convenience extras? Roadside assistance and repair network benefits can tip toward comprehensive.

Examples (two short case studies)

Case A: Ali, 10-year-old sedan, city parking

Ali owns a 10-year-old sedan with modest resale value. He parks on the street and wants to save on premiums. He can repair minor dents himself. He chooses third-party, saves on annual premiums, and keeps an emergency fund for repairs. Risk: if the car is stolen or totaled, Ali’s out-of-pocket cost would be high.

Case B: Sara, new compact hatchback on finance

Sara bought a 2-year-old hatchback on loan and commutes daily through high-traffic areas. Her bank requires comprehensive cover. She chooses comprehensive with zero-depreciation and roadside assistance to reduce repair bills and avoid disrupting commuting. Premiums are higher but the financial protection aligns with her needs.

Tips to lower comprehensive premiums without losing cover

-

Increase the voluntary deductible (if you can afford it in a claim).

-

Install anti-theft devices and parking sensors; declare secure parking.

-

Maintain a clean driving record to build NCB.

-

Bundle policies (home + auto) if insurer offers discounts.

-

Compare multiple insurers and negotiate — different companies price risk differently.

-

Opt for a limited set of relevant add-ons rather than buying every available rider.

Frequently asked questions (short)

Q: Will comprehensive payout be the invoice price of my car?

A: Usually you receive market value at the time of loss, not the original invoice. GAP/return-to-invoice covers the shortfall if you want invoice value protection.

Q: Does comprehensive include collision?

A: Not always. Some comprehensive policies include collision; others list collision separately. Always check policy details.

Q: Does third-party protect me if the other driver is uninsured?

A: No — third-party protects others from you. If you need protection from uninsured-at-fault drivers, look for uninsured/underinsured motorist coverage or consider comprehensive packages that include such options.

Final verdict — which is better?

There is no single “better” option. It depends entirely on your car’s value, your financial resilience, local risks, legal requirements, and personal preference.

-

Third-party is better when: budget is the primary constraint, the car is of low value, and you accept bearing your own repair/replacement risk.

-

Comprehensive is better when: your car is newer or valuable, you want peace of mind against theft/fire/natural disasters, you have a finance company requiring it, or you simply prefer lower financial uncertainty.

A practical middle path: if your car’s value is borderline, you might run third-party while setting aside a dedicated emergency fund sized to cover a plausible repair/replacement. If you lean toward comprehensive but want to cut premiums, customize your policy with a higher deductible and only the add-ons you need.

Closing — make the choice intentionally

Insurance is not just about price — it’s risk management. The “right” policy protects what you can’t easily replace or afford to lose. Read policy wordings, compare quotes, understand deductibles and exclusions, and pick the plan that aligns with your finances and peace of mind. If you want, I can help compare sample quotes, create a checklist of questions to ask insurers in your area, or draft an email you can send to multiple insurers to request customized quotes.