Auto insurance is not just a legal necessity in most countries—it is also one of the most important financial protections you can invest in as a vehicle owner. Whether you’re a first-time car buyer or someone renewing a policy, understanding how auto insurance works and what factors to consider can save you money, reduce stress, and ensure that you’re adequately protected in case of an accident.

In this guide, we’ll break down the top 10 things to know before buying auto insurance, so you can make an informed decision and choose the best policy for your needs.

1. Understand the Basics of Auto Insurance

Before you dive into policy shopping, it’s crucial to understand what auto insurance actually is and how it works.

At its core, auto insurance is a contract between you and an insurance company. You pay a premium, and in return, the insurer promises to cover certain costs related to accidents, theft, or damage to your car, depending on your policy type.

The main components of auto insurance include:

-

Liability coverage: Pays for injuries or property damage you cause to others.

-

Collision coverage: Pays for damage to your car caused by accidents, regardless of fault.

-

Comprehensive coverage: Covers non-collision-related damages, such as theft, fire, or natural disasters.

-

Uninsured/underinsured motorist coverage: Protects you if you’re hit by someone without sufficient insurance.

-

Personal injury protection (PIP) or medical payments: Helps cover medical expenses for you and your passengers.

Having this foundation will help you evaluate policies and decide what coverage you need versus what’s optional.

2. Know the Legal Requirements in Your State or Country

Auto insurance requirements vary widely depending on where you live. Some regions mandate only liability coverage, while others require additional protections like personal injury protection (PIP) or uninsured motorist coverage.

For example:

-

In the United States, almost every state requires some level of liability insurance.

-

In Canada, provinces may mandate both liability and accident benefits.

-

In the UK and many parts of Europe, at least third-party insurance is mandatory.

Failing to meet the legal requirements can result in penalties, license suspension, or even jail time. Always check the minimum coverage laws in your area, but remember: minimum coverage often isn’t enough to protect you financially in a serious accident.

3. Assess Your Coverage Needs

While meeting the legal minimum is necessary, it’s often not sufficient. To decide how much coverage you really need, ask yourself:

-

How much would it cost to repair or replace my vehicle if it were totaled?

-

Do I live in an area prone to natural disasters, theft, or vandalism?

-

How much could I afford out of pocket in case of an accident?

-

Do I frequently drive in high-traffic or high-risk areas?

If you have an older car with little market value, you may skip comprehensive and collision coverage. On the other hand, if you own a new or expensive vehicle, full coverage is usually worth the cost.

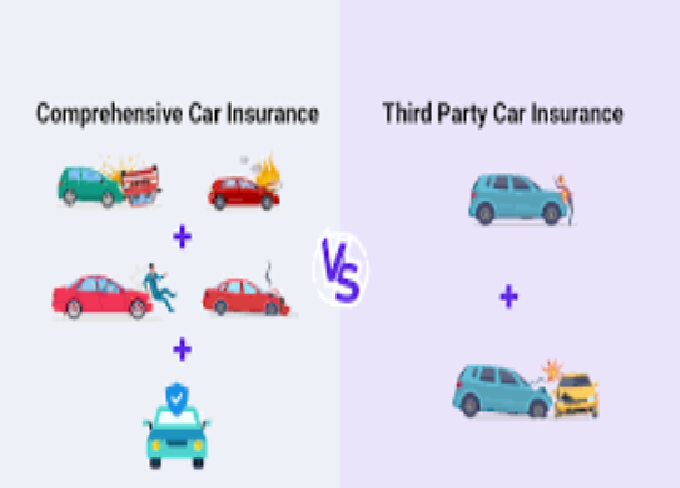

4. Compare Different Types of Policies

Auto insurance isn’t one-size-fits-all. The three most common policy types are:

-

Liability-only (third-party insurance): Cheapest, but only covers damages you cause to others.

-

Collision and comprehensive (full coverage): More expensive but covers your own vehicle as well.

-

Usage-based or pay-as-you-drive policies: Premiums depend on driving behavior, tracked via telematics devices or apps.

Comparing these options will help you balance affordability and protection. For most drivers, full coverage provides peace of mind, especially for newer cars.

5. Shop Around and Compare Quotes

One of the biggest mistakes buyers make is settling for the first insurance quote they receive. Different insurers calculate risk differently, so the same driver could be quoted very different premiums by multiple companies.

When shopping around:

-

Get at least three to five quotes from different providers.

-

Use online comparison tools to save time.

-

Don’t just compare prices—compare coverage, deductibles, and add-ons too.

Remember, the cheapest policy isn’t always the best. Focus on value for money and reliability of the insurer.

6. Understand How Premiums Are Calculated

Knowing what affects your premium helps you make smarter choices. Insurers typically consider:

-

Driving history: Accidents, tickets, and claims increase premiums.

-

Age and gender: Younger drivers, especially males, usually pay more.

-

Location: Urban areas with higher accident/theft rates lead to higher costs.

-

Type of car: Luxury or sports cars cost more to insure than standard sedans.

-

Credit score (in some countries): Poor credit can result in higher premiums.

-

Annual mileage: The more you drive, the higher the risk.

By understanding these factors, you can take proactive steps to reduce your premium, such as improving your driving record or opting for a safer car.

7. Decide on Deductibles Wisely

The deductible is the amount you agree to pay out of pocket before your insurance kicks in. For example, if you have a $500 deductible and cause $2,000 worth of damage, you’ll pay $500 while the insurer covers $1,500.

Choosing a higher deductible usually lowers your premium, but it also means paying more upfront in case of an accident. A lower deductible makes claims easier but raises monthly costs.

The key is to find a balance: choose a deductible you can comfortably afford in case of an emergency.

8. Look for Discounts and Savings Opportunities

Insurance companies often offer discounts that can significantly lower your premium. Common discounts include:

-

Safe driver discounts: For maintaining a clean driving record.

-

Multi-policy discounts: Bundling auto with home or renters insurance.

-

Good student discounts: For students with high grades.

-

Low mileage discounts: For drivers who don’t drive much annually.

-

Safety feature discounts: Cars with airbags, anti-theft systems, or ABS brakes may qualify.

Always ask your insurer what discounts are available. Sometimes, small adjustments—like installing anti-theft devices or completing a defensive driving course—can save you hundreds annually.

9. Evaluate the Insurance Company’s Reputation

Price isn’t everything when it comes to auto insurance. The insurer’s reliability is just as important. Before purchasing a policy, research:

-

Customer service ratings: How easy is it to contact them in emergencies?

-

Claim settlement ratio: Do they pay claims promptly and fairly?

-

Financial strength: Are they stable enough to handle large-scale claims?

-

Online reviews and recommendations: Feedback from real customers can reveal red flags.

Choosing a reputable company ensures peace of mind that your claims will be handled efficiently when you need them most.

10. Read the Policy Fine Print Carefully

Many policyholders discover gaps in their coverage only after filing a claim. To avoid surprises, read the policy terms and conditions carefully before signing.

Pay attention to:

-

Exclusions: What isn’t covered (e.g., wear and tear, using the car for commercial purposes).

-

Limits of liability: The maximum the insurer will pay for damages.

-

Add-ons or riders: Optional extras like roadside assistance, rental reimbursement, or zero-depreciation coverage.

-

Cancellation terms: Your rights to cancel and possible penalties.

If you’re unsure about any clause, ask your insurer for clarification. It’s better to understand the policy upfront than to be disappointed later.

Bonus Tip: Review Your Policy Regularly

Auto insurance isn’t a one-time decision. Your circumstances can change—buying a new car, moving to a new city, or improving your credit score could all affect your rates. Reviewing your policy annually helps you adjust coverage, drop unnecessary add-ons, or switch insurers if better options become available.

Conclusion

Buying auto insurance may seem overwhelming, but with the right knowledge, you can make smart decisions that protect both your car and your finances. To recap, the top 10 things to know before buying auto insurance are:

-

Understand the basics of auto insurance.

-

Know your state or country’s legal requirements.

-

Assess your personal coverage needs.

-

Compare different types of policies.

-

Shop around for quotes.

-

Learn how premiums are calculated.

-

Choose deductibles wisely.

-

Take advantage of discounts.

-

Research the insurer’s reputation.

-

Read the fine print thoroughly.

By keeping these factors in mind, you’ll not only stay compliant with the law but also secure the best possible protection at a price that fits your budget. Remember: auto insurance isn’t just about protecting your car—it’s about protecting your financial future and peace of mind.