Life insurance is often seen as just another financial product, but in reality, it plays a pivotal role in shaping an individual’s overall financial security and long-term wealth strategy. It goes beyond providing financial support after death — it helps safeguard families, preserve wealth, manage taxes, and even create opportunities for future growth. In this detailed guide, we will explore how life insurance fits into financial planning, why it is essential for wealth protection, and how individuals can make informed decisions when integrating it into their financial strategies.

Understanding Life Insurance

What is Life Insurance?

Life insurance is a contract between an individual (policyholder) and an insurance company. In exchange for regular premium payments, the insurer provides a lump sum payment (death benefit) to the policyholder’s beneficiaries upon their death.

The key purpose of life insurance is to replace lost income, cover expenses, and ensure financial stability for dependents. However, certain types of policies also serve as investment and wealth accumulation tools, making them versatile instruments in financial planning.

Types of Life Insurance

There are several types of life insurance policies, each serving different financial needs:

-

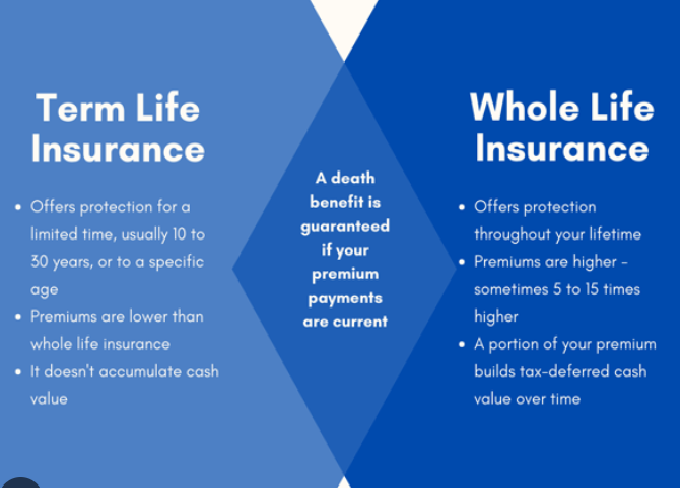

Term Life Insurance – Provides coverage for a specific period (e.g., 10, 20, or 30 years). It is affordable and straightforward but does not build cash value.

-

Whole Life Insurance – Offers lifelong coverage with fixed premiums and a guaranteed cash value component that grows over time.

-

Universal Life Insurance – Provides flexibility in premium payments and death benefits, with a cash value component tied to market interest rates.

-

Variable Life Insurance – Allows policyholders to invest the cash value in sub-accounts, offering growth potential but with higher risk.

-

Indexed Universal Life Insurance – Links cash value growth to stock market indices, balancing risk and reward.

Why Life Insurance is a Cornerstone of Financial Planning

1. Income Replacement and Family Protection

The most fundamental role of life insurance is income replacement. If a family’s primary breadwinner passes away, life insurance ensures that dependents are not left struggling to pay for daily expenses, education, healthcare, or outstanding debts.

For example, a young family with small children may rely heavily on one parent’s salary. Without insurance, the sudden loss of that income could be devastating. With adequate coverage, however, the surviving family members can maintain their standard of living.

2. Debt and Liability Management

Life insurance helps pay off outstanding debts, such as mortgages, car loans, personal loans, or credit card balances. This prevents dependents from inheriting financial burdens. For business owners, life insurance can also help settle business debts or fund buy-sell agreements.

3. Education and Long-Term Goals

Life insurance can be structured to ensure that long-term goals, such as children’s education or marriage expenses, are funded even in the absence of the insured. Some policies also accumulate cash value, which can be accessed during the policyholder’s lifetime to help finance these goals.

4. Peace of Mind

Financial planning isn’t only about numbers — it’s also about peace of mind. Knowing that loved ones will be financially protected allows individuals to live with less stress and more confidence in their financial journey.

The Wealth Protection Aspect of Life Insurance

Life insurance is not just a safety net; it is also a tool for wealth preservation and estate planning.

1. Estate Planning and Wealth Transfer

For high-net-worth individuals, life insurance helps transfer wealth efficiently to the next generation. The death benefit is usually tax-free for beneficiaries, making it an effective estate planning tool. It can cover estate taxes, ensuring that heirs don’t have to liquidate assets to meet tax obligations.

2. Asset Protection

In many jurisdictions, life insurance proceeds are protected from creditors, meaning that beneficiaries receive the payout even if the policyholder had outstanding liabilities. This ensures wealth is preserved for the family rather than being consumed by debts.

3. Business Continuity

Business owners often use life insurance to ensure continuity. Policies can fund buy-sell agreements, compensate for the loss of key employees, and provide liquidity to maintain business operations after a sudden death.

4. Retirement and Wealth Accumulation

Certain permanent life insurance policies build cash value, which grows tax-deferred. Policyholders can borrow against this cash value or withdraw funds to supplement retirement income. Unlike other investment vehicles, these withdrawals are often tax-advantaged.

Tax Advantages of Life Insurance

Life insurance offers multiple tax benefits, making it a powerful financial planning tool:

-

Tax-Free Death Benefit – The payout to beneficiaries is usually exempt from income tax.

-

Tax-Deferred Growth – Cash value in permanent policies grows without annual taxation.

-

Tax-Advantaged Loans and Withdrawals – Policyholders can access cash value through loans, often without triggering taxable events.

-

Estate Tax Mitigation – Properly structured life insurance policies can reduce estate tax liabilities.

Integrating Life Insurance into Financial Planning

1. Assessing Financial Needs

The first step is evaluating how much coverage is necessary. This depends on income, debts, dependents, and future goals. A common method is the “income replacement approach”, which multiplies annual income by the number of years the family would need support.

2. Balancing Insurance and Investments

While life insurance is important, it should be balanced with other financial priorities like retirement savings, emergency funds, and investments. For some, term insurance paired with aggressive investment in mutual funds or real estate may be better than whole life policies.

3. Choosing the Right Policy

Each policy type suits different situations:

-

Young families – Term life for affordable coverage.

-

Wealthy individuals – Whole or universal life for estate planning.

-

Business owners – Key person insurance or buy-sell funding policies.

4. Reviewing Regularly

Life insurance needs evolve with life stages. Marriage, children, home purchase, or business expansion all affect coverage requirements. Regular policy reviews ensure the coverage stays relevant.

Life Insurance in Different Life Stages

1. Young Professionals

Even if young individuals have no dependents, life insurance can lock in lower premiums and provide a foundation for future financial planning.

2. Married Couples and Families

This stage often carries the highest financial responsibilities — mortgages, children’s education, and lifestyle costs. Adequate term coverage is crucial here.

3. Mid-Life and Pre-Retirement

As children grow and debts decrease, coverage may shift from income replacement to wealth protection and retirement planning. Permanent life insurance with cash value accumulation becomes more attractive.

4. Retirement and Legacy Planning

During retirement, life insurance ensures a smooth transfer of wealth to heirs, covers estate taxes, and may even provide supplemental income through cash value access.

Common Misconceptions About Life Insurance

-

“I don’t need life insurance if I’m young.”

– In reality, premiums are lowest when young and healthy, making it the best time to buy. -

“Term insurance is a waste because it doesn’t build cash value.”

– While it doesn’t build cash value, term insurance offers the highest coverage at the lowest cost, serving its purpose effectively. -

“My employer-provided life insurance is enough.”

– Employer policies often provide limited coverage (1–2 years of salary) and do not transfer if you change jobs. -

“Life insurance is only for the wealthy.”

– Life insurance benefits families across all income levels by protecting dependents and covering financial liabilities.

Case Studies: Life Insurance in Action

Case Study 1: Income Protection for a Young Family

Ali, a 35-year-old professional, purchased a 20-year term life policy worth $200,000. After his unexpected death, the payout covered his mortgage, children’s school fees, and daily living expenses, ensuring his wife and children were financially secure.

Case Study 2: Business Continuity

Sana and Ahmed co-owned a small business. They each bought life insurance policies naming the other as a beneficiary to fund a buy-sell agreement. When Ahmed passed away, Sana used the payout to buy his share from his heirs, keeping the business running.

Case Study 3: Estate Planning

A wealthy retiree structured a whole life policy in a trust for his grandchildren. Upon his death, the policy payout bypassed probate, avoided estate taxes, and provided a lasting legacy for his family.

Challenges and Considerations

-

High Premium Costs – Permanent policies can be expensive compared to term insurance.

-

Complexity of Products – Many policies come with riders, investment features, and varying terms, making them confusing for buyers.

-

Inflation Risk – Fixed death benefits may lose real value over decades unless inflation-adjusted.

-

Policy Lapse – If premiums are not paid, policies can lapse, leading to a loss of coverage.

Practical Tips for Buying Life Insurance

-

Start early to lock in low premiums.

-

Determine the right amount of coverage using financial calculators.

-

Compare policies from multiple insurers.

-

Work with a trusted financial advisor.

-

Regularly update beneficiaries.

-

Reassess coverage after major life events.

The Future of Life Insurance in Financial Planning

With advancements in technology, digital platforms, and personalized products, life insurance is becoming more accessible and tailored. Insurtech companies are introducing faster underwriting, AI-based premium pricing, and flexible policies that adapt to changing lifestyles.

Moreover, with growing financial literacy, people are beginning to view life insurance not just as a safety net but as a strategic tool for wealth management.

Conclusion

Life insurance is far more than a death benefit — it is a cornerstone of financial planning and wealth protection. From replacing income and securing dependents’ futures to preserving estates and supplementing retirement, life insurance provides stability, peace of mind, and long-term value.

By understanding different types of policies, integrating them wisely into financial plans, and regularly reviewing coverage, individuals can harness the full power of life insurance. Whether you are just starting your financial journey or planning your legacy, life insurance ensures that your wealth, values, and vision live on for generations.