Life insurance often seems complex and overwhelming, especially for those who are new to financial planning. Between different policy types, terms, premiums, riders, and exclusions, it’s easy to feel lost. However, life insurance is one of the most important financial products you can purchase—it provides protection for your loved ones, ensures financial security, and can even act as a long-term investment tool.

This beginner’s guide is designed to break down life insurance in simple terms. By the end, you’ll understand the basics of how life insurance works, the different types of policies, how to choose the right one, and what mistakes to avoid.

What is Life Insurance?

Life insurance is a contract between you and an insurance company. You pay regular premiums, and in return, the insurer promises to pay a lump sum of money (called the death benefit) to your beneficiaries upon your death.

The core purpose of life insurance is to provide financial support to your loved ones when you are no longer there to take care of them. It ensures that expenses such as mortgage payments, daily living costs, debts, or children’s education can be covered.

Why Life Insurance Matters

Many people underestimate the value of life insurance, thinking it’s unnecessary if they are young or healthy. However, life is unpredictable, and having financial protection in place is a smart move.

Key Reasons Life Insurance is Important:

-

Income Replacement – Your family relies on your income for daily needs. Life insurance ensures they won’t struggle financially in your absence.

-

Debt Repayment – Outstanding loans or mortgages can be paid off, preventing financial burden.

-

Children’s Future – Education expenses and life milestones can be covered.

-

Final Expenses – Funeral and medical costs are managed without draining savings.

-

Wealth Creation – Certain policies also offer investment opportunities to build long-term wealth.

How Does Life Insurance Work?

The concept is simple:

-

You purchase a policy from an insurance company.

-

You pay premiums (monthly, quarterly, or yearly).

-

If you pass away during the policy term, the insurance company pays a death benefit to your beneficiaries.

Example:

Suppose you buy a policy with a $200,000 death benefit and pay $30 per month. If you pass away unexpectedly, your family will receive the $200,000, even if you only paid a few months of premiums.

Types of Life Insurance Policies

Life insurance isn’t one-size-fits-all. Policies differ based on duration, features, and benefits. Let’s look at the most common types:

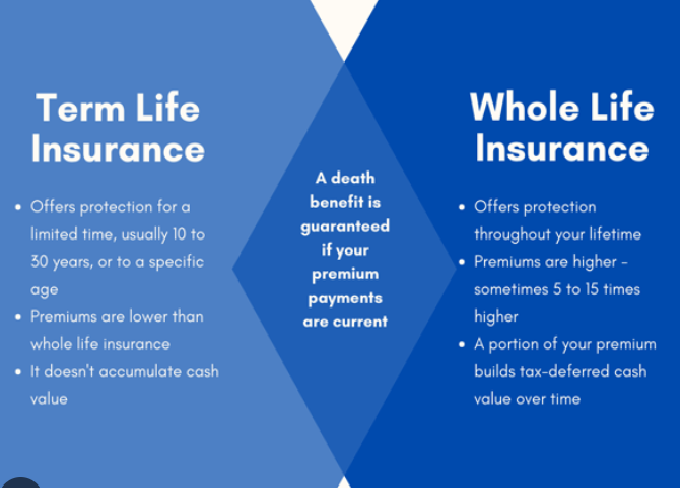

1. Term Life Insurance

-

Definition: Coverage for a fixed period (10, 20, or 30 years).

-

Features:

-

Affordable premiums.

-

Pure protection—no savings or investment.

-

If you survive the term, no payout.

-

-

Best For: Young families, people with limited budgets, or those seeking high coverage at a low cost.

2. Whole Life Insurance

-

Definition: Permanent coverage that lasts your entire life.

-

Features:

-

Higher premiums than term insurance.

-

Guaranteed death benefit.

-

Builds cash value over time (you can borrow against it).

-

-

Best For: Long-term planners who want both protection and investment.

3. Universal Life Insurance

-

Definition: Flexible permanent insurance with adjustable premiums and death benefits.

-

Features:

-

Builds cash value.

-

You can increase or decrease coverage as needed.

-

Premiums may vary depending on market conditions.

-

-

Best For: People seeking flexibility and long-term investment growth.

4. Variable Life Insurance

-

Definition: A policy that allows you to invest cash value into sub-accounts (like mutual funds).

-

Features:

-

Higher risk, but also higher growth potential.

-

Cash value depends on investment performance.

-

-

Best For: Experienced investors willing to take risks for potential rewards.

5. Group Life Insurance

-

Definition: Life insurance provided by employers or associations.

-

Features:

-

Usually free or low-cost.

-

Coverage ends when you leave the job.

-

-

Best For: Employees looking for temporary, low-cost coverage.

Key Components of a Life Insurance Policy

When reviewing a life insurance policy, pay attention to these important components:

-

Premiums – The amount you pay regularly (monthly or yearly).

-

Death Benefit – The lump sum your beneficiaries receive.

-

Policy Term – Duration of coverage (for term policies).

-

Cash Value – A savings component in permanent policies.

-

Beneficiary – The person(s) who will receive the payout.

-

Riders – Optional add-ons for extra benefits.

Common Riders in Life Insurance

Riders enhance your policy for specific needs:

-

Accidental Death Benefit Rider – Extra payout if death occurs due to an accident.

-

Critical Illness Rider – Lump sum payment if diagnosed with major illnesses.

-

Waiver of Premium Rider – Waives premiums if you become disabled.

-

Child Term Rider – Provides coverage for children under the policy.

-

Return of Premium Rider – Refunds premiums if you outlive the policy term.

Factors That Affect Life Insurance Premiums

Insurance companies calculate your premiums based on risk factors:

-

Age – Younger applicants pay lower premiums.

-

Health – Pre-existing conditions or poor health raise costs.

-

Lifestyle – Smoking, drinking, or dangerous hobbies increase premiums.

-

Occupation – High-risk jobs (e.g., construction, mining) cost more.

-

Policy Type & Term – Permanent policies are more expensive than term policies.

-

Coverage Amount – Higher coverage means higher premiums.

How Much Coverage Do You Need?

The amount of life insurance you need depends on your financial situation.

General Rule of Thumb:

-

10 to 15 times your annual income.

Factors to Consider:

-

Outstanding debts (mortgage, loans).

-

Family’s living expenses.

-

Children’s education costs.

-

Future inflation.

-

Final expenses.

Steps to Buying a Life Insurance Policy

-

Assess Your Needs – Calculate how much coverage you require.

-

Understand Policy Types – Choose between term or permanent insurance.

-

Compare Providers – Check different companies’ offerings and customer reviews.

-

Get Multiple Quotes – Premiums vary; shop around before deciding.

-

Read Policy Details Carefully – Understand exclusions, terms, and conditions.

-

Take a Medical Exam (if required) – Insurers may ask for health tests.

-

Buy Early – The younger you are, the cheaper the premiums.

Common Mistakes to Avoid

-

Underestimating Coverage Needs – Buying too little coverage leaves your family underprotected.

-

Delaying Purchase – Waiting until older increases premiums.

-

Not Comparing Policies – Different insurers offer different rates.

-

Ignoring Riders – Missing out on valuable additional protection.

-

Failing to Review Policy Regularly – Life changes require coverage adjustments.

-

Relying Only on Employer Coverage – Group insurance often isn’t enough.

Frequently Asked Questions (FAQs)

Q1: Do I need life insurance if I’m single?

Yes. Even if you don’t have dependents, life insurance can cover debts, funeral costs, and leave something for loved ones.

Q2: Can I buy life insurance without a medical exam?

Yes, many insurers offer “no exam” policies, but they may be more expensive.

Q3: What happens if I miss a premium payment?

Most policies have a grace period (30–31 days). If you don’t pay within that time, the policy may lapse.

Q4: Can I change beneficiaries later?

Yes, you can update beneficiaries anytime.

Q5: Is life insurance taxable?

In most countries, death benefits are tax-free. However, check local regulations.

Reviewing and Updating Your Policy

Life circumstances change—marriage, children, buying a home, or career growth. Review your policy every few years to ensure it still meets your needs. You may need to increase coverage or add riders as your financial responsibilities grow.

Life Insurance as an Investment Tool

Some permanent policies (whole life, universal life, variable life) not only provide protection but also act as investment vehicles. The cash value grows over time and can be used for:

-

Retirement income supplement.

-

Emergency funds.

-

Collateral for loans.

However, always remember that the primary purpose of life insurance is protection, not investment.

Conclusion

Life insurance is a cornerstone of financial planning, offering peace of mind that your loved ones will be taken care of in your absence. While policies can seem complicated at first, understanding the basics—types, coverage needs, and key features—makes decision-making easier.

For beginners, term life insurance is often the best starting point due to its affordability and simplicity. As your financial situation evolves, you can consider permanent policies or add riders for additional security.

The key is to start early, assess your needs carefully, and choose a reputable insurer. By doing so, you not only safeguard your family’s financial future but also take a crucial step toward long-term financial stability.