Auto insurance is not just a legal requirement in most countries but also a financial safeguard that protects you, your vehicle, and others on the road. With hundreds of insurance companies offering different policies, choosing the best one for your car can feel overwhelming. The “best” policy isn’t always the cheapest—it’s the one that balances cost, coverage, customer service, and reliability.

This article provides a complete guide on how to choose the right auto insurance policy for your car, what to look for, and common mistakes to avoid.

Why Auto Insurance Matters

Before diving into the selection process, it’s important to understand why auto insurance is essential:

-

Legal Requirement: In most regions, driving without insurance is illegal. At minimum, liability coverage is mandatory.

-

Financial Protection: Insurance saves you from paying out-of-pocket for accidents, theft, or natural disasters.

-

Peace of Mind: Knowing you’re covered in emergencies reduces stress while driving.

-

Third-Party Liability: Protects you from lawsuits and damages you may cause to others.

Having the right insurance means you’re financially secure, legally compliant, and more confident on the road.

Step 1: Assess Your Insurance Needs

The first step to choosing the right policy is to understand your specific requirements. Consider the following:

-

Car’s Age and Value: New or expensive cars usually need comprehensive coverage, while older vehicles may only require liability.

-

Driving Habits: Do you drive long distances daily or occasionally? High-mileage drivers face more risk.

-

Location: If you live in an area prone to accidents, theft, or natural disasters, you’ll need broader coverage.

-

Budget: Decide how much you can afford for premiums without compromising your financial stability.

-

Personal Risk Tolerance: If you prefer peace of mind, a comprehensive plan is better; if you’re okay with taking risks, a basic plan works.

Step 2: Understand the Types of Auto Insurance Coverage

Before comparing policies, learn the different types of coverage available:

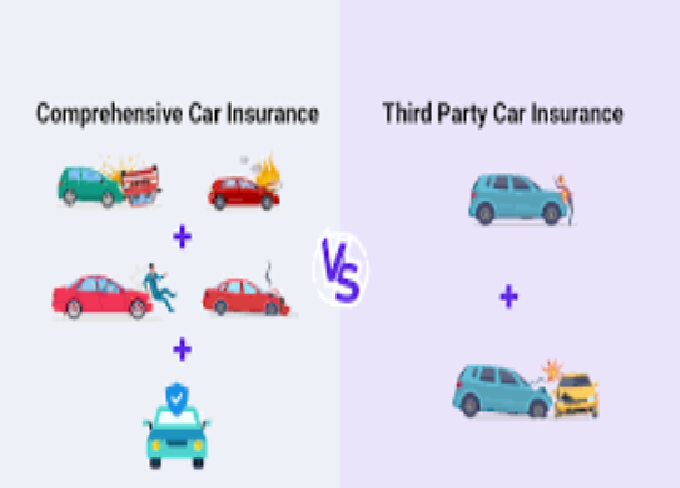

1. Liability Insurance

-

Covers damages or injuries you cause to others.

-

Mandatory in most places.

-

Does not cover your own vehicle.

2. Collision Coverage

-

Pays for damages to your car after a collision, regardless of fault.

-

Essential for new cars.

3. Comprehensive Coverage

-

Covers theft, fire, vandalism, floods, and natural disasters.

-

Recommended if your car is expensive or if you live in risk-prone areas.

4. Personal Injury Protection (PIP)

-

Covers medical expenses for you and your passengers after an accident.

-

Some countries/states require it by law.

5. Uninsured/Underinsured Motorist Coverage

-

Protects you if the at-fault driver has little or no insurance.

6. Add-ons & Riders

-

Roadside assistance, zero depreciation, rental reimbursement, and gap insurance are optional add-ons that can enhance your coverage.

Understanding these options ensures you don’t overpay for unnecessary features or end up underinsured.

Step 3: Compare Insurance Providers

Once you know what coverage you need, the next step is to compare insurers. Focus on:

-

Reputation & Financial Strength: Check ratings from agencies like A.M. Best or Standard & Poor’s to ensure the company can pay claims.

-

Customer Reviews: Look for feedback on claims settlement speed, transparency, and customer support.

-

Coverage Options: Some companies specialize in comprehensive packages, while others focus on budget-friendly policies.

-

Discounts Offered: Safe driver, multi-car, anti-theft device, and good student discounts can save money.

-

Accessibility: A company with a strong online presence, mobile app, or 24/7 helpline is more convenient.

Step 4: Compare Premiums and Deductibles

Many drivers make the mistake of choosing the cheapest policy. Instead, you should balance premiums with deductibles.

-

Premiums: The fixed amount you pay monthly or annually. Lower premiums may mean limited coverage.

-

Deductibles: The out-of-pocket amount you pay before insurance kicks in. Higher deductibles lower premiums but increase personal risk.

Pro Tip: Choose a deductible that balances affordability and risk. Don’t pick a deductible so high that you can’t afford it during an accident.

Step 5: Check the Claim Settlement Ratio

The claim settlement ratio (CSR) is the percentage of claims an insurer settles compared to total claims filed.

-

High CSR = Reliable insurer.

-

Low CSR = Higher risk of delayed or denied claims.

Always prioritize insurers with a strong track record of settling claims quickly and fairly.

Step 6: Look for Policy Flexibility

Life changes—so should your insurance. Choose an insurer that allows:

-

Adding/removing coverage mid-term.

-

Adjusting deductibles.

-

Adding new drivers to the policy.

-

Switching cars without canceling coverage.

Flexibility ensures that your policy remains useful even as your circumstances evolve.

Step 7: Don’t Overlook Exclusions

Insurance policies always have exclusions—situations they don’t cover. Common exclusions include:

-

Driving under the influence of alcohol/drugs.

-

Intentional accidents or fraud.

-

Using a personal car for commercial purposes.

-

War, riots, or nuclear risks.

Read the fine print carefully to avoid unpleasant surprises during claims.

Step 8: Take Advantage of Discounts

Most insurers offer discounts to help reduce premiums. Some common ones include:

-

No-Claim Bonus (NCB): Reward for not filing claims in the previous year.

-

Multi-Policy Discount: If you bundle auto, home, and health insurance.

-

Loyalty Discounts: For long-term customers.

-

Safety Features: Cars with airbags, ABS, and anti-theft devices often qualify.

-

Good Driver Discount: Clean driving record = lower premiums.

Always ask your insurer about available discounts before finalizing a policy.

Step 9: Consider Your Driving Record

Your driving history significantly affects premiums.

-

Clean Record: Lower premiums, higher discounts.

-

Frequent Accidents or Tickets: Higher premiums due to increased risk.

If you have a poor record, consider insurers specializing in high-risk drivers. Alternatively, maintain safe driving habits for a year or two to qualify for lower rates later.

Step 10: Evaluate Customer Service

Insurance is more than just coverage—it’s also about support when you need it most. Test an insurer’s customer service by:

-

Calling their helpline.

-

Asking about policy details.

-

Checking response times via email or chat.

Companies that provide quick, transparent, and helpful responses are usually reliable during emergencies.

Common Mistakes to Avoid When Choosing Auto Insurance

-

Only Looking at Price: Cheapest doesn’t always mean best. Balance affordability with coverage.

-

Not Reading the Fine Print: Ignoring exclusions can lead to denied claims.

-

Skipping Add-ons: Sometimes, small add-ons like roadside assistance can save big money in emergencies.

-

Not Comparing Enough Providers: Comparing at least 3–5 insurers ensures better deals.

-

Failing to Update Policies: Not updating after moving, buying a new car, or changing driving habits can lead to gaps in coverage.

When to Re-Evaluate Your Auto Insurance Policy

Even after purchasing, regularly review your policy. You should re-evaluate when:

-

Buying a new or used car.

-

Moving to a new city or state.

-

Adding/removing drivers.

-

Experiencing life changes (marriage, retirement, etc.).

-

Premiums increase significantly.

Regular reviews ensure your coverage remains relevant and affordable.

Tips to Save Money on Auto Insurance

-

Shop around every year for better deals.

-

Increase deductibles if financially feasible.

-

Install anti-theft devices in your car.

-

Bundle multiple insurance policies.

-

Maintain a good credit score (where applicable).

-

Avoid small, unnecessary claims to preserve your no-claim bonus.

Conclusion

Choosing the best auto insurance policy for your car requires careful research and consideration. Start by evaluating your needs, understanding different coverage options, and comparing insurers. Don’t just focus on price—look at claim settlement ratios, exclusions, customer service, and flexibility. Remember, the right insurance policy isn’t just a legal requirement—it’s a financial shield that protects you, your family, and your vehicle.

By following the steps outlined in this guide, you can confidently select an auto insurance policy that provides maximum protection at the best value.