Life insurance is one of the most reliable financial tools for ensuring long-term security for your loved ones. It provides a death benefit to your beneficiaries, helping them cope with financial challenges when you are no longer around. However, life insurance policies are not always one-size-fits-all. Every individual has different needs, lifestyles, and financial goals. This is where life insurance riders come into play.

Riders are add-on provisions or optional benefits that can be attached to a base life insurance policy. They allow you to customize your coverage by addressing specific risks or circumstances that might not be covered under a standard plan. Whether it’s covering critical illnesses, providing income in case of disability, or protecting your children’s future, riders enhance the overall value of your life insurance policy.

This article explores in detail what life insurance riders are, their types, their importance, and how they can help you create a more comprehensive financial safety net.

What Are Life Insurance Riders?

A life insurance rider is an amendment or addition to your base policy that provides extra benefits or flexibility. Instead of buying multiple separate policies, riders let you adjust your coverage according to your needs. For example, if you are concerned about the financial impact of a serious illness, you can add a critical illness rider to receive a lump sum upon diagnosis.

Riders are optional and typically come with an additional cost, but they are often much cheaper than purchasing a separate standalone policy for the same coverage. Think of riders as customizable upgrades that enhance the protection offered by your life insurance plan.

Why Life Insurance Riders Matter

You may wonder: if a standard life insurance policy already provides financial protection, why add riders? Here are some key reasons why riders matter:

-

Tailored Protection – Riders allow you to design coverage that reflects your personal risks and circumstances.

-

Cost-Effective – Riders are usually less expensive compared to buying a separate policy.

-

Flexibility – They let you modify or enhance your coverage at different stages of life.

-

Financial Security Beyond Death – Some riders provide benefits during your lifetime, not just after death.

-

Peace of Mind – Riders cover unexpected situations like accidents, illnesses, or disabilities that could otherwise disrupt your family’s finances.

Common Types of Life Insurance Riders

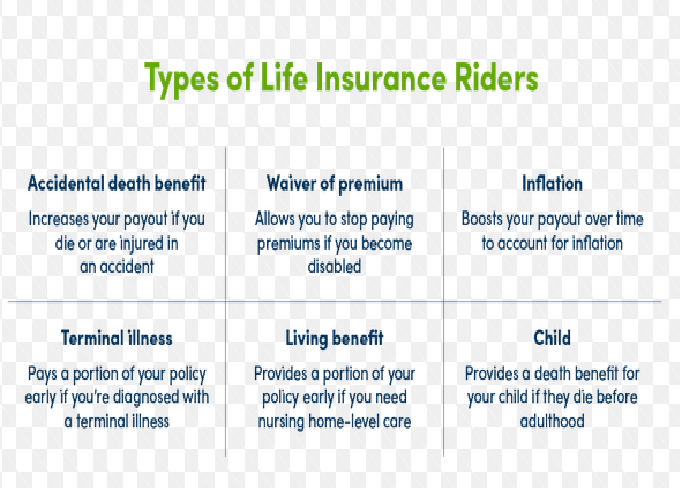

1. Accidental Death Benefit Rider

This rider provides an additional payout if the insured dies due to an accident. For example, if your base policy covers $500,000 and you have a $200,000 accidental death rider, your beneficiaries will receive $700,000 in the event of an accidental death.

Why It Matters: It is useful for individuals in high-risk professions or those frequently exposed to accident-prone environments.

2. Waiver of Premium Rider

If the policyholder becomes totally disabled and cannot work, this rider waives future premium payments while keeping the policy active.

Why It Matters: It ensures your life insurance coverage remains intact even if you lose the ability to pay due to disability.

3. Critical Illness Rider

This rider provides a lump sum benefit if the policyholder is diagnosed with a specified critical illness such as cancer, heart attack, or stroke.

Why It Matters: Medical expenses and loss of income during a severe illness can be overwhelming. This rider offers immediate financial relief.

4. Accelerated Death Benefit Rider

This rider allows the policyholder to access a portion of the death benefit while still alive if diagnosed with a terminal illness.

Why It Matters: It helps cover medical bills, long-term care, or other urgent expenses in the final stage of life.

5. Disability Income Rider

With this rider, if you become disabled and unable to work, the insurance company provides a monthly income for a specified period.

Why It Matters: It acts as a replacement income stream, ensuring your family’s financial stability even when you can’t earn.

6. Child Term Rider

This rider provides coverage for your children under the parent’s life insurance policy. If the child passes away, a death benefit is paid out.

Why It Matters: It offers financial support for funeral costs or other unexpected expenses while giving parents peace of mind.

7. Long-Term Care Rider

This rider allows you to use a portion of the death benefit to pay for long-term care services if you are unable to perform daily living activities (e.g., bathing, dressing, eating).

Why It Matters: Long-term care can be very expensive, and this rider helps cover those costs without depleting family savings.

8. Return of Premium Rider

If you outlive your policy term, this rider ensures that all the premiums you paid are returned to you.

Why It Matters: It provides a sense of security, as you don’t feel like your premiums are “wasted” if you survive the term.

9. Spouse Rider

This rider extends coverage to your spouse under the same policy.

Why It Matters: It can be a cost-effective way to ensure both partners are covered without buying two separate policies.

10. Guaranteed Insurability Rider

This rider allows you to purchase additional coverage in the future without undergoing medical examinations.

Why It Matters: It is ideal for young policyholders who expect increased financial responsibilities (marriage, children, mortgages) later in life.

Advantages of Life Insurance Riders

-

Personalized Coverage – Choose riders that reflect your health risks, family situation, and career.

-

Affordable Add-Ons – Riders usually cost less than standalone insurance products.

-

Financial Protection While Living – Some riders like critical illness or disability income support you during your lifetime.

-

Tax Benefits – In many countries, rider premiums may qualify for tax deductions (depending on local laws).

-

Peace of Mind – Knowing you are protected from multiple risks provides emotional and financial stability.

Disadvantages and Limitations of Riders

While riders are beneficial, they are not without limitations:

-

Extra Cost – Adding multiple riders can significantly increase your premium.

-

Complexity – Too many riders can make your policy complicated to manage.

-

Limited Coverage – Riders usually cover specific events only; they are not substitutes for comprehensive insurance.

-

Eligibility Restrictions – Some riders require medical exams or are unavailable after a certain age.

How to Choose the Right Riders

1. Assess Your Needs

Consider your health, career risks, and family responsibilities. For example, if you have a family history of critical illnesses, a critical illness rider is wise.

2. Compare Costs

Evaluate whether the extra premium for a rider is affordable and justified.

3. Check Policy Terms

Carefully read the exclusions, limitations, and waiting periods attached to riders.

4. Consider Future Needs

Opt for riders like guaranteed insurability if you expect your responsibilities to grow in the future.

5. Consult a Financial Advisor

A professional can help align riders with your long-term financial plan.

Real-Life Example: The Value of Riders

Consider this scenario:

-

Ali, a 35-year-old father of two, buys a life insurance policy worth $500,000.

-

He adds three riders: waiver of premium, critical illness, and child term.

At age 42, Ali is diagnosed with a critical illness. The critical illness rider pays him $100,000, which he uses for treatment and living expenses. Since he can no longer work, the waiver of premium rider ensures he doesn’t have to pay premiums. If tragedy strikes and he passes away, his family will still receive the $500,000 death benefit, plus coverage for his children under the child term rider.

This case shows how riders turn a standard policy into a comprehensive safety net.

Life Insurance Riders vs. Separate Policies

A common question is whether it’s better to buy riders or separate standalone policies.

-

Riders are cost-effective, convenient, and customizable but may offer limited coverage.

-

Separate Policies provide broader and more flexible coverage but are usually more expensive.

The choice depends on your budget and the level of protection you need.

The Future of Life Insurance Riders

The insurance industry is evolving rapidly with digital tools, personalized plans, and increasing consumer demand for flexibility. We can expect more innovative riders, such as:

-

Wellness Riders – Offering discounts or benefits for maintaining a healthy lifestyle.

-

Mental Health Riders – Covering therapy or treatment expenses.

-

Pandemic Riders – Designed to cover risks arising from global health crises.

These trends suggest that riders will continue to play an increasingly important role in creating tailored insurance solutions.

Conclusion

Life insurance riders are powerful tools that transform a standard life insurance policy into a personalized protection plan. They cover situations beyond just death, such as accidents, disabilities, critical illnesses, or long-term care needs. While they come with extra costs and some limitations, their value in providing customized, affordable, and comprehensive coverage is undeniable.

When chosen wisely, riders can make the difference between a basic life insurance policy and a complete financial shield for you and your family. Whether you are looking for additional security, cost savings, or future flexibility, understanding and leveraging life insurance riders is essential for effective financial planning.