Life insurance is one of the most important financial tools you can purchase to protect your loved ones. It acts as a safety net, ensuring that in the event of your passing, your family is not left struggling financially. But when you start researching life insurance, you quickly realize that there are different types available—most notably term life insurance and whole life insurance.

Both options come with advantages, disadvantages, and unique features that cater to different needs and financial situations. Choosing the right one depends on your goals, budget, and long-term plans. This article will break down the differences between term and whole life insurance, their pros and cons, and help you decide which policy is right for you.

Understanding Life Insurance Basics

Before diving into term versus whole life, it’s essential to understand what life insurance is at its core. Life insurance is a contract between you and an insurance company. You pay regular premiums, and in exchange, the insurer promises to pay a lump sum (called the death benefit) to your beneficiaries upon your passing.

The primary purpose of life insurance is financial protection. It can cover expenses like:

-

Mortgage payments

-

Children’s education

-

Daily living costs for dependents

-

Funeral and medical expenses

-

Debt repayment

While the end goal is the same—protecting your family—how policies work differs greatly between term life and whole life.

What Is Term Life Insurance?

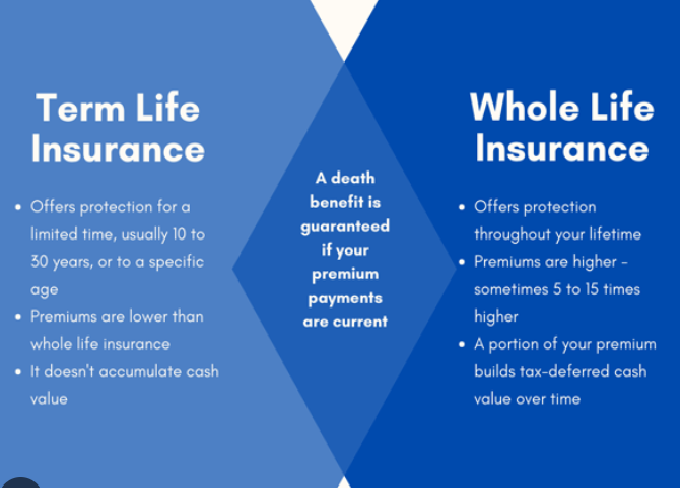

Term life insurance provides coverage for a set period of time, known as the “term.” Common terms are 10, 20, or 30 years. If you pass away during the policy term, your beneficiaries receive the death benefit. However, if you outlive the term, the policy expires, and no benefit is paid.

Key features of term life insurance:

-

Affordable premiums compared to whole life

-

Coverage for a specific period (not permanent)

-

No cash value component (pure protection)

-

Renewable or convertible options may be available

Term life is straightforward: it’s designed to cover you during the years when your family is most financially vulnerable—such as when raising kids, paying off a mortgage, or building savings.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance. Unlike term life, it provides lifelong coverage as long as you keep paying your premiums. In addition to a death benefit, whole life policies also include a cash value component—a savings feature that grows over time on a tax-deferred basis.

Key features of whole life insurance:

-

Lifelong coverage (does not expire)

-

Fixed premiums that never increase

-

Cash value accumulation that you can borrow against or withdraw

-

Acts as both insurance and a financial investment tool

Whole life insurance is often chosen by individuals who want guaranteed coverage, estate planning benefits, or a way to leave a legacy.

Comparing Term vs. Whole Life Insurance

Now let’s break down the differences more clearly.

1. Coverage Duration

-

Term Life: Temporary (10–30 years). Best for covering specific obligations like a mortgage or child-rearing years.

-

Whole Life: Permanent (lifelong). Best for estate planning or those who want guaranteed lifelong protection.

2. Premium Costs

-

Term Life: Much cheaper—especially for younger, healthy individuals. Premiums only increase if you renew after the term ends.

-

Whole Life: Significantly more expensive because it includes lifelong protection and cash value savings.

3. Cash Value

-

Term Life: No savings or investment component. Pure protection.

-

Whole Life: Builds cash value that grows over time. You can borrow against it or use it as collateral.

4. Flexibility

-

Term Life: Some policies are renewable or convertible to whole life, but flexibility is limited.

-

Whole Life: Offers long-term financial flexibility through cash value access, but premiums are rigid.

5. Death Benefit

-

Term Life: Pays out only if you die during the policy term.

-

Whole Life: Pays out whenever you die, as long as premiums are paid.

Pros and Cons of Term Life Insurance

✅ Pros:

-

Affordable: Allows you to purchase high coverage at low cost.

-

Simple: Easy to understand, no complex investment features.

-

Flexible Coverage: Perfect for specific financial obligations like mortgage, education, or debt protection.

❌ Cons:

-

Temporary: Coverage ends when the term expires.

-

No Cash Value: You don’t build savings or investments.

-

Rising Costs at Renewal: Premiums can increase dramatically if you renew at an older age.

Pros and Cons of Whole Life Insurance

✅ Pros:

-

Lifelong Coverage: Guarantees payout regardless of when you die.

-

Cash Value Growth: Builds a tax-deferred savings fund.

-

Fixed Premiums: Payments remain the same for life.

-

Estate Planning Benefits: Useful for leaving an inheritance or covering estate taxes.

❌ Cons:

-

Expensive: Premiums are 5–15 times higher than term life.

-

Complex: Includes savings features that may be confusing.

-

Lower Returns: Cash value grows slowly compared to other investments.

When Term Life Insurance Is Right for You

Term life insurance may be the right choice if:

-

You’re young and want affordable coverage.

-

You need coverage for a specific time frame (e.g., until kids graduate or mortgage is paid).

-

You’re focused on maximum coverage at minimum cost.

-

You plan to invest separately and don’t need insurance as an investment tool.

Example: A 30-year-old parent buys a 20-year term policy for $500,000. If they die during the policy period, their family gets financial support. If they outlive it, they can renew or let it expire once financial responsibilities are reduced.

When Whole Life Insurance Is Right for You

Whole life insurance may be the right choice if:

-

You want lifelong coverage.

-

You’re interested in building a tax-deferred cash value.

-

You have long-term estate planning goals.

-

You can afford higher premiums without financial strain.

Example: A 40-year-old buys a whole life policy with $250,000 coverage. Over time, they build cash value they can borrow against. When they pass away—even decades later—their beneficiaries are guaranteed a payout.

Cost Comparison: Term vs. Whole Life

Let’s look at a quick comparison based on average premium estimates (these vary by age, health, and insurer):

-

30-Year-Old Male (Healthy, Non-Smoker)

-

$500,000 Term (20 years): $20–30/month

-

$500,000 Whole Life: $300–500/month

-

-

40-Year-Old Female (Healthy, Non-Smoker)

-

$500,000 Term (20 years): $35–50/month

-

$500,000 Whole Life: $400–600/month

-

This shows how much more costly whole life is compared to term.

Common Misconceptions

-

“Whole life is always better because it lasts forever.”

Not necessarily—many people don’t need lifelong coverage. Once kids are independent and debts are paid, a large policy may no longer be necessary. -

“Term life is wasted money if you outlive it.”

Not true—think of it like car or health insurance. You don’t complain if you don’t “use” it; it served its purpose by protecting you when needed. -

“Cash value in whole life is the same as investment returns.”

False—returns are usually modest. For higher growth, separate investments (stocks, retirement funds) are often better.

Hybrid Options: Universal and Variable Life Insurance

In addition to term and whole life, there are hybrid products like:

-

Universal Life Insurance: Flexible premiums and adjustable death benefit, with cash value growth tied to interest rates.

-

Variable Life Insurance: Allows investment in sub-accounts (like mutual funds), offering higher risk and reward.

These can provide more flexibility but are also more complex and riskier.

How to Decide: Key Questions to Ask Yourself

-

What’s my budget?

If cost is your primary concern, term life is the clear winner. -

Do I need coverage for life or just a period?

If you only need coverage for 20–30 years, term life is sufficient. -

Am I interested in cash value savings?

If yes, whole life (or another permanent policy) may suit you. -

What are my financial goals?

-

Building wealth separately? → Term life.

-

Estate planning and legacy goals? → Whole life.

-

-

Will I outgrow my policy?

Consider how your financial responsibilities will change over time.

Expert Recommendations

-

Financial advisors often recommend term life for most people because it provides high coverage at low cost. The money saved on premiums can then be invested in higher-return vehicles like retirement accounts.

-

Whole life insurance is best for high-net-worth individuals, those with estate planning needs, or people who want guaranteed lifelong coverage.

Final Thoughts

Choosing between term and whole life insurance is not a one-size-fits-all decision. Term life insurance offers affordable, straightforward protection for a set period, making it ideal for most families who want financial security during their working years. Whole life insurance, on the other hand, provides lifelong protection and a cash value component, but at a much higher cost.

The right choice depends on your goals, budget, and financial responsibilities. For many, a term policy plus disciplined investing may be the smarter option. For others—especially those seeking estate planning benefits or guaranteed lifelong coverage—whole life could be worth the higher premiums.

Ultimately, the best policy is the one that aligns with your family’s needs and gives you peace of mind knowing your loved ones will be protected.