Health is the most valuable asset of life, but it is also the most unpredictable. No one knows when an accident, illness, or medical emergency might occur. Healthcare costs around the world are rising steadily, and even routine checkups, tests, and minor procedures can create financial strain. In such an environment, health insurance acts as a shield that protects both your health and your financial stability.

This article explains what health insurance is, how it works, its key components, and why it is essential for every individual and family.

Understanding Health Insurance

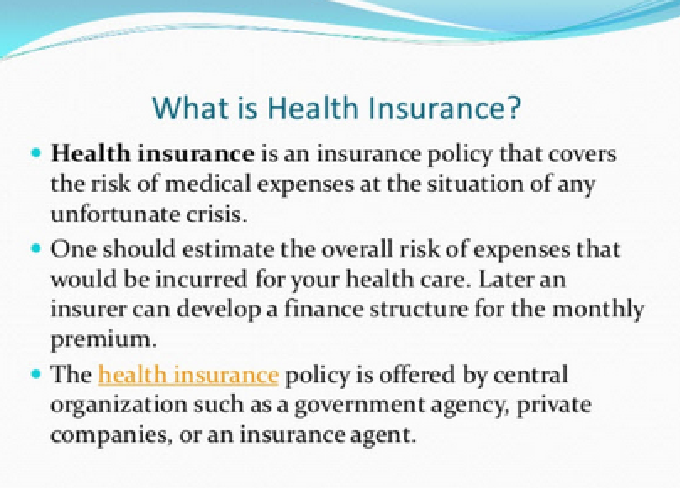

At its core, health insurance is a contract between an individual (the policyholder) and an insurance company. The policyholder pays a regular amount called a premium, and in return, the insurance company covers certain medical expenses. These can include doctor visits, hospital stays, medications, surgeries, preventive care, and more, depending on the type of plan.

In simple words, health insurance ensures that you don’t have to bear the entire financial burden of healthcare by yourself. Instead, the insurer shares that responsibility.

How Does Health Insurance Work?

Health insurance operates on the principle of risk-sharing. Since no one can predict who will fall sick or require medical attention, insurance companies pool together premiums from many policyholders. When someone within that pool needs medical care, the insurance fund is used to pay for their treatment.

Here’s how the process typically works:

-

Premium Payment – You pay a monthly, quarterly, or yearly premium to keep your health insurance active.

-

Coverage – The insurance company defines what expenses are covered. This may include hospitalization, outpatient care, preventive services, maternity care, dental or vision (depending on the plan).

-

Deductibles and Co-payments – Some policies require you to pay a certain amount out of pocket before insurance starts covering expenses. After that, the insurer pays the larger share.

-

Network Hospitals/Providers – Many insurers have agreements with hospitals and clinics (known as “network providers”). Visiting these providers usually means lower costs.

-

Claims Process – When you receive medical treatment, the hospital may bill the insurer directly (cashless claim) or you may pay first and then file for reimbursement.

Types of Health Insurance Plans

Health insurance isn’t one-size-fits-all. There are different types of plans to meet different needs:

1. Individual Health Insurance

Covers a single person for medical expenses. Ideal for individuals without dependents.

2. Family Floater Plan

Covers an entire family under one plan. A single premium provides coverage for all family members, which is usually more economical than buying separate policies.

3. Group Health Insurance

Often provided by employers, these plans cover employees and sometimes their dependents. Premiums are usually lower since risks are spread across a larger group.

4. Critical Illness Insurance

Provides a lump sum amount if you are diagnosed with a critical illness like cancer, stroke, or heart attack. Useful for managing expensive treatments.

5. Maternity and Newborn Insurance

Covers medical expenses related to childbirth and newborn care.

6. Senior Citizen Health Insurance

Specifically designed for older adults, these plans provide coverage for age-related illnesses and typically offer higher coverage for hospitalizations.

Key Features of Health Insurance

Understanding the features of a health insurance policy helps in making better choices. Some common features include:

-

Sum Insured – The maximum amount the insurance company will cover in a year.

-

Cashless Facility – Direct settlement with hospitals, so you don’t have to pay large amounts upfront.

-

Pre and Post-Hospitalization – Expenses incurred before admission and after discharge are often covered.

-

Daycare Procedures – Modern treatments that do not require 24-hour hospitalization may also be covered.

-

Renewability – Lifetime renewability ensures you stay covered as you age.

-

Tax Benefits – Premiums paid are often eligible for tax deductions (depending on local tax laws).

Why Do You Need Health Insurance?

Now that we’ve understood what health insurance is and how it functions, let’s explore why it is necessary.

1. Protection Against Rising Healthcare Costs

Medical inflation is real. The cost of treatment, hospital stays, medicines, and surgeries is increasing every year. Health insurance protects you from the financial shock of these rising expenses.

2. Covers Unexpected Medical Emergencies

Accidents, sudden illnesses, or critical health conditions can strike at any time. Having health insurance means you can access quality care without worrying about draining your savings.

3. Access to Better Healthcare Facilities

With insurance, you are more likely to choose reputed hospitals and doctors, ensuring better treatment. Many policies also provide cashless hospitalization, making emergency admissions easier.

4. Financial Security for Your Family

A health crisis affects the whole family. Insurance ensures that your loved ones are protected financially, reducing stress during difficult times.

5. Encourages Preventive Care

Many health insurance plans cover preventive checkups, vaccinations, and screenings. This promotes early detection of diseases, reducing long-term medical costs and improving health outcomes.

6. Tax Benefits

In many countries, health insurance premiums qualify for tax deductions. This means you not only secure your health but also save money.

7. Coverage for Critical Illnesses

Specialized plans provide coverage for life-threatening conditions. Without insurance, such treatments could be financially devastating.

8. Peace of Mind

Knowing that you and your family are covered allows you to live with confidence. Health insurance reduces the financial anxiety associated with medical uncertainties.

Common Myths About Health Insurance

Many people avoid buying insurance because of misconceptions. Let’s clear some common myths:

-

Myth 1: I am young and healthy, so I don’t need insurance.

Fact: Illnesses and accidents can happen at any age. Buying insurance early means lower premiums. -

Myth 2: Health insurance is too expensive.

Fact: Basic plans are affordable, and the cost is far less than a hospital bill. -

Myth 3: Employer-provided insurance is enough.

Fact: Employer coverage often ends when you switch jobs and may not be adequate for family needs. -

Myth 4: Pre-existing conditions are never covered.

Fact: Many insurers cover them after a waiting period.

Factors to Consider When Choosing a Health Insurance Plan

When selecting a policy, keep these factors in mind:

-

Coverage Amount (Sum Insured) – Should be sufficient to cover potential hospital expenses in your city.

-

Network Hospitals – Ensure your preferred hospitals are on the insurer’s list.

-

Waiting Periods – Especially for pre-existing conditions and maternity coverage.

-

Exclusions – Read the fine print to know what is not covered.

-

Premium vs Benefits – Cheapest isn’t always best. Balance cost with coverage.

-

Add-Ons (Riders) – Options like critical illness cover or accidental death benefit can enhance protection.

The Global Perspective on Health Insurance

Health insurance systems vary globally:

-

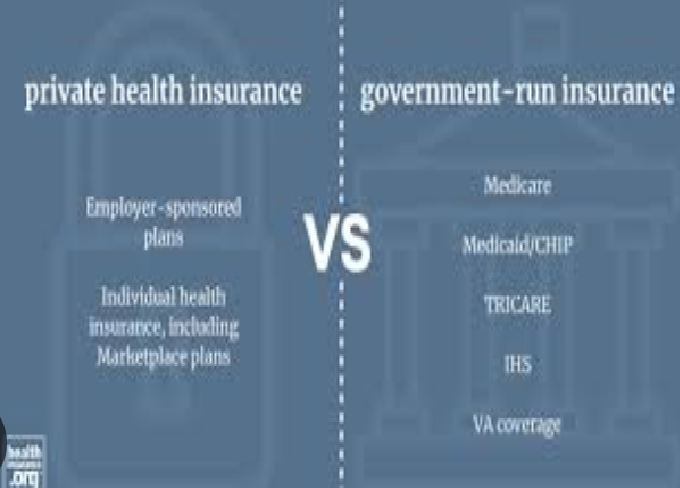

United States – Health insurance is often tied to employment, with private insurers playing a major role. Government programs like Medicare and Medicaid cover specific groups.

-

Europe – Many countries follow universal healthcare, funded by taxes, but private insurance can supplement coverage.

-

Asia – Countries like India and Pakistan are witnessing growing awareness of private health insurance, though public healthcare remains an option.

-

Middle East – In some nations, health insurance is mandatory for residents and expatriates.

Despite these differences, the need for financial protection against healthcare costs is universal.

The Long-Term Benefits of Health Insurance

Looking beyond immediate needs, health insurance provides lasting benefits:

-

Builds a Safety Net – Over years, insurance protects against multiple health risks.

-

Helps in Retirement Planning – With rising age, medical needs increase, making insurance critical in old age.

-

Supports Overall Financial Planning – Reduces the need to liquidate assets during health crises.

Conclusion

Health insurance is not just a financial product; it is an essential part of responsible living. By covering medical costs, it ensures access to quality healthcare, protects your savings, and provides peace of mind. In today’s uncertain world, health insurance is not a luxury—it is a necessity.

Whether you are young and single, married with children, or approaching retirement, there is a plan tailored for your needs. The sooner you invest in health insurance, the greater the benefits you and your family will enjoy.